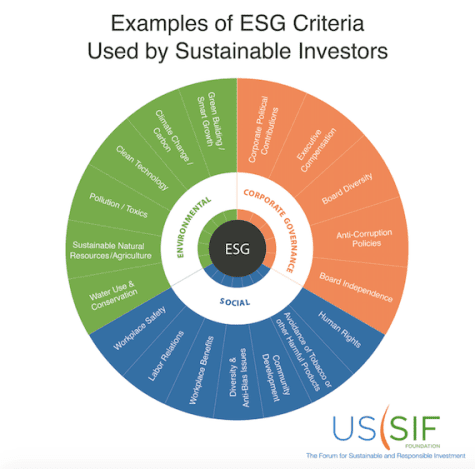

Here at AFM we’ve always been concerned with, and in some cases involved in, promoting positive social issues and sustainable, environmentally friendly practices. Given that these topics have been dominating politics and the news headlines as of late, we feel it’s a perfect time to highlight and explain the differences between two rapidly growing investment strategies; environmental, social, & governance (ESG) and sustainable, responsible, & impact (SRI). There are many similarities between the two, and the terms are often used interchangeably, but their objectives can be very different. The integration of ESG factors looks at the environmental, social, & governance practices of an investment to determine if they could have a material impact on the performance, which is used to enhance traditional financial analysis by identifying potential opportunities and risks beyond technical valuations. The image below provides common factors for the three areas of ESG that are often considered.

Although there is a connection to social improvements, the main objective of ESG evaluation is financial performance and these strategies are primarily concerned with how an investment’s ESG score will impact its returns.

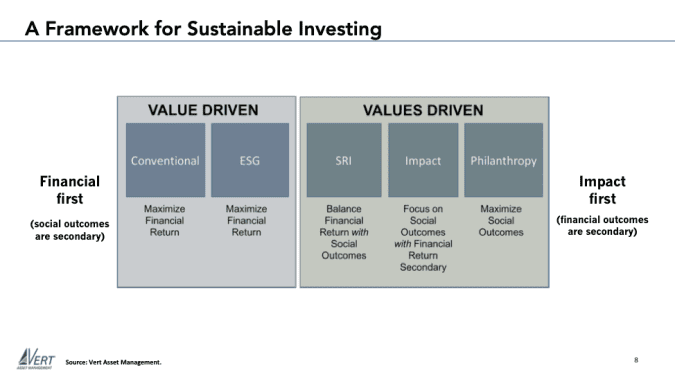

SRI in its original form went one step further and was a way for investors to avoid companies based on some negative ESG factor that they disliked about the company. The underlying motive could be religion, personal values or political beliefs; among other things. This is now known as “exclusions” or “negative-screen” investing, as additional SRI strategies have since been developed. One that has become very popular of late is “impact investing,” where investors provide capital to innovative companies or projects that are working to solve some of the world’s most important problems. An important segment known as “community investing,” works explicitly to finance projects and institutions that benefit poor and underserved communities in the U.S. and overseas. With impact investing there is even less of a focus on financial return. The infographic below illustrates some meaningful distinctions between the different sustainable investing strategies.

SECTOR GROWTH AND PERFORMANCE

According to the US SIF Foundation (The US Forum for Sustainable and Responsible Investing), US-domiciled assets under management (AUM) using SRI investing strategies grew from $8.7 trillion at the start of 2016 to $12.0 trillion at the start of 2018, a 38% increase. Of the $46.6 trillion in assets under professional management in the U.S., roughly 26%, or slightly more than one out of every four dollars is involved in SRI. They first started measuring total U.S. SRI assets in 1995 which were $639 billion at that time, and since then total assets have grown at a compound annual growth rate of 13.6%.

Initially there was some underperformance for sustainable investment strategies, which was partially the result of investor confusion that led to lower demand than traditional strategies. However, as ESG factors have become more prevalent in the news and increasingly popular among certain demographics (Millennials in particular), the demand for these strategies has grown rapidly. There are now multiple studies that indicate no statistical difference in SRI returns compared to broad market benchmarks over the long term, and in some cases they even suggested a small performance advantage. According to a 2015 meta-study conducted by Oxford University and Arabesque Partners that reviewed over 200 sources, “80 percent of the reviewed studies demonstrate that prudent sustainability practices have a positive influence on investment performance.”

When you think about the individual companies whose stock (or bonds) these SRI strategies would be investing in, studies have found that those with strong sustainability and sound management practices largely demonstrate better operational performance, which ultimately translates into cash flows. Additionally, because these companies are committed to higher standards, they normally have less risk of running into legal issues from wrongful practices and have less volatile performance.

THE FINAL WORD

The demand and growth of sustainable & responsible investing in the U.S. is showing no signs of slowing down anytime soon. Although these investment strategies aren’t suitable for everyone, we’re focused on building our expertise in these areas to better serve our clients. We are in the process of updating our recommended ESG & SRI investment lists and our benchmark portfolios to incorporate those options. Please let us know if you’re interested in trying to incorporate more ESG and SRI focused investments into your portfolio, or if you’d like to discuss these topics further.

*Socially responsible investing involves the exclusion of certain securities for nonfinancial reasons. This may result in the investor forgoing some market opportunities that may have been available to those not subject to such criteria. There is no guarantee that any investment goal will be met.

Presented by Mitch Strobel, CFP®