For many retirees and those nearing retirement, health care is one of the biggest financial concerns. Medicare provides an important foundation, but it doesn’t cover everything. From routine care to prescription drugs and long-term support, understanding your coverage options and planning ahead can help you manage costs, protect your savings, and reduce stress. This guide outlines the essentials you need to take control of health care expenses in retirement.

Understanding Medicare and Other Insurance Options

After you retire, you’ll typically transition away from employer-sponsored health insurance. For most people, Medicare becomes the primary source of coverage beginning the month they turn 65. It’s crucial to understand what Medicare includes, what it doesn’t, and to enroll on time. Delaying enrollment in Medicare Part B or Part D can result in late-enrollment penalties that may last for life.

The Parts of Medicare

Medicare coverage is divided into several parts:

- Part A (Hospital Insurance)

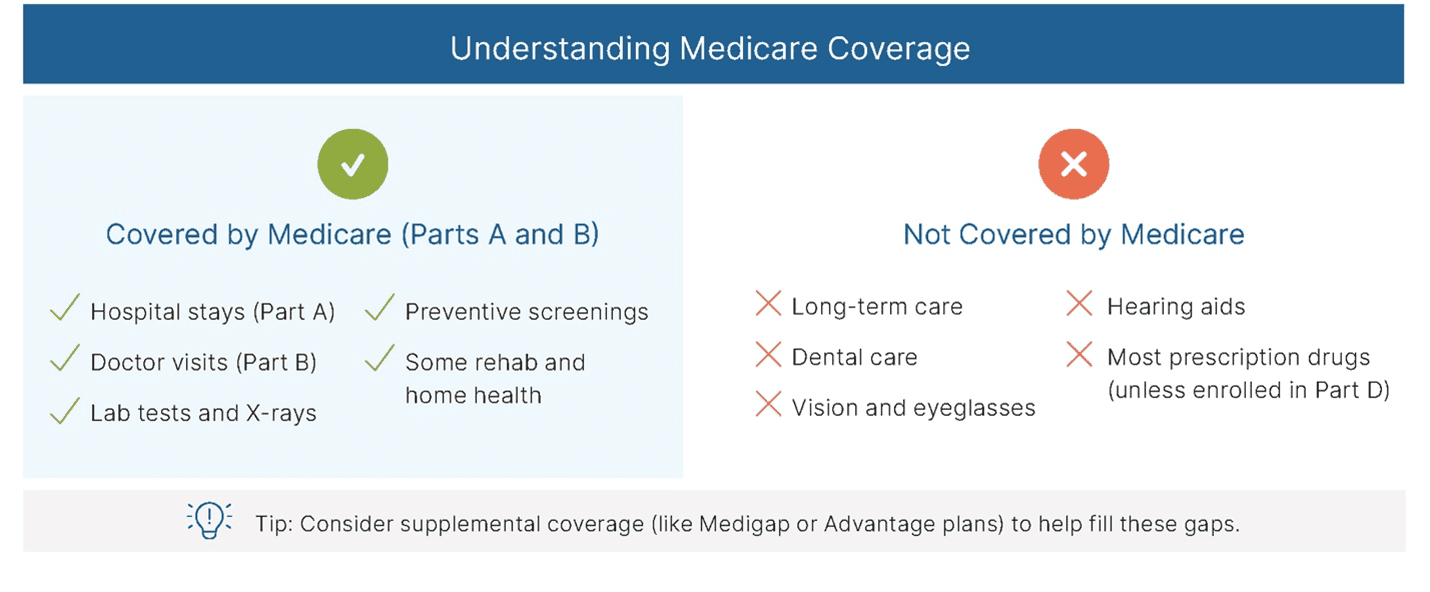

Covers inpatient hospital care and is often premium-free if you paid Medicare taxes while working. - Part B (Medical Insurance)

Covers doctor visits, outpatient care, and many preventive services. Part B requires a monthly premium. - Part D (Prescription Drug Coverage)

Helps cover prescription drugs through a separate plan, or through a Medicare Advantage plan that includes drug coverage. - Medicare Advantage (Part C)

An alternative to Original Medicare, offered by private insurers. These plans bundle Parts A and B (and often Part D) and may include additional benefits such as dental, vision, hearing, and wellness programs. In exchange, they typically use provider networks and may have different rules for referrals and out-of-pocket costs.

Filling the Gaps: Medigap vs. Medicare Advantage

Original Medicare (Parts A and B) does not cover everything. It generally excludes routine dental care, eye exams, hearing aids, and most long-term care services. It also leaves you responsible for deductibles and coinsurance. To help manage these costs, many retirees choose either a Medigap (Medicare Supplement) policy or a Medicare Advantage plan:

- Medigap (Medicare Supplement) policies

Work alongside Original Medicare to help cover out-of-pocket costs such as copayments, coinsurance, and deductibles. Medigap plans do not include prescription drug coverage, so you’ll typically need a separate Part D plan. You also have a guaranteed-issue right to buy certain Medigap policies—meaning insurers can’t deny coverage or charge more due to health history—during the first six months after enrolling in Part B (at age 65 or older). - Medicare Advantage plans

These plans replace Original Medicare with an all-in-one option. They may include extra benefits and lower premiums, but they can restrict which doctors and hospitals you can use and may come with different cost-sharing rules.

If You Retire Before Age 65

If you retire before you’re eligible for Medicare, you’ll need interim coverage. Common options include:

- Health Insurance Marketplace plans

- COBRA continuation coverage (often expensive and usually limited to up to 18 months, which may not fully bridge the gap to Medicare eligibility)

- Retiree health benefits from a former employer (if available)

Medicaid as a Backstop

For retirees with limited income and resources, Medicaid may provide additional support. Because Medicaid is administered jointly by federal and state governments, eligibility and benefits vary by state. Importantly, Medicaid can cover long-term care services that Medicare generally does not. In some cases, individuals may need to spend down assets to qualify. If Medicaid may be part of your long-term plan, it can be helpful to speak with a financial advisor or an elder law attorney.

Reducing Out-of-Pocket Health Care Expenses

Even with solid coverage, retirement healthcare expenses, including premiums, deductibles, copays, and coinsurance, can add up quickly. The good news is there are practical ways to reduce these costs:

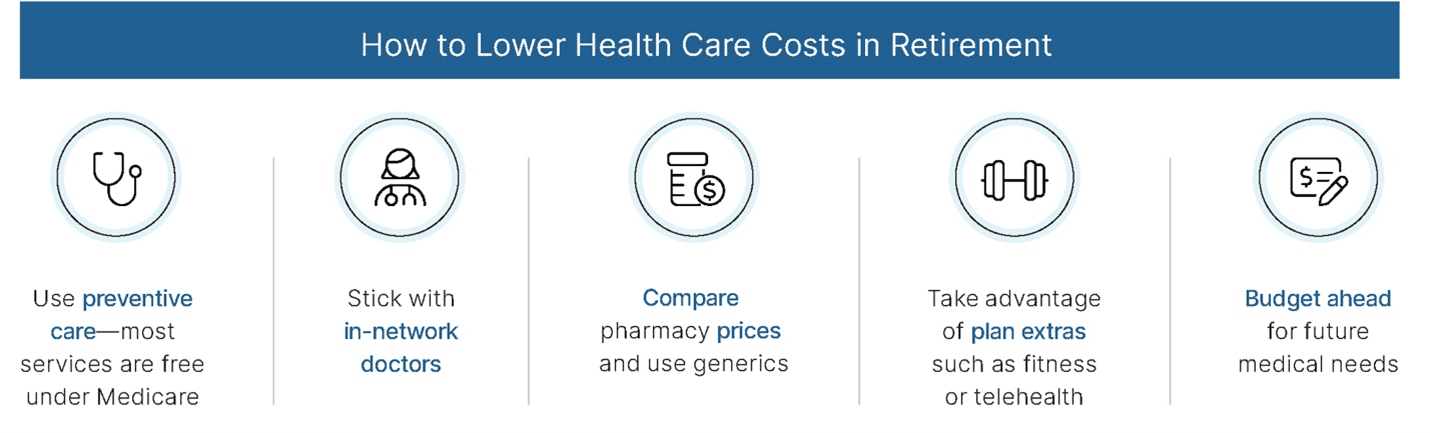

- Use preventive care benefits

Medicare covers many preventive services such as annual wellness visits, screenings, and vaccines, at no additional cost. Preventive care can catch issues early and help avoid more expensive complications later. - Stay in-network when it matters

If you enroll in a Medicare Advantage plan (or have other coverage that uses networks), choosing in-network doctors and facilities can reduce costs and help prevent surprise bills. - Be strategic about prescriptions

Drug prices can vary dramatically. Compare pharmacy prices, ask about generic alternatives, and confirm that your medications are included on your plan’s formulary (preferred drug list). - Use available “extra” benefits

Many Medicare Advantage plans include benefits such as telehealth access, wellness programs, gym memberships, or chronic condition support. Used well, these benefits can improve health and reduce downstream costs. - Build health care into your retirement budget

Plan for premiums and predictable out-of-pocket costs and leave room for the unexpected. If you have a Health Savings Account (HSA) from working years, those funds can be used tax-free for qualified medical expenses in retirement. Once you’re enrolled in any part of Medicare, including Part A, you can no longer contribute to an HSA, but the balance remains yours to use.

Smart coverage decisions plus proactive health habits can go a long way toward reducing costs and increasing peace of mind.

Don’t Overlook Long-Term Care

Long-term care includes help with everyday activities such as bathing, dressing, and eating—whether at home, in assisted living, or in a nursing facility. Many people need some form of long-term care at some point, yet Medicare generally does not cover most long-term care services. Without planning, long-term care expenses can place significant strain on retirement savings. Common approaches include:

- Paying out of pocket using savings and income

- Purchasing long-term care insurance, often most affordable and accessible in your 50s or early 60s

- Planning for potential Medicaid eligibility, especially for those with limited resources or significant long-term care risk

Health status plays a major role in long-term care insurance eligibility, so applying earlier—before serious conditions develop—can improve your chances and potentially lower premiums. A financial advisor can help you weigh these options and map a strategy that fits your needs and values.

Closing Thought

By understanding your Medicare choices, planning for long-term care, and using proven strategies to reduce out-of-pocket costs, you can protect your financial security and focus more fully on enjoying retirement. If you’re unsure how to tailor a plan to your situation, a trusted financial advisor can help you build clarity—without the jargon.

© 2025 Commonwealth Financial Network®

Presented by Carl Holubowich, CFP®