The Federal Reserve cut interest rates by 0.50% in mid-September, the first rate cut since they began raising rates in late 2022 to combat inflation. At the outset of 2024 it was expected that cuts would begin in the spring, but the Fed took a cautious approach, waiting until they were certain inflation was under control. Now that we’ve seemingly accomplished that goal, the Fed appears to be on a path to further rate cuts later this year and into 2025.

While the Fed doesn’t directly set consumer rates for things like mortgages, the target rate is used as a reference point across a broad swath of the economy and the world. Below we examine how changes to the target rate ripple out across the stock, bond, lending markets, and more.

Stocks

When it comes to the stock market, rate cuts can be a Jekyll or Hyde situation. In a vacuum, lower rates cuts are positive for stocks. Lower rates means lower borrowing costs for both business and consumers, making companies more profitable and giving consumers more disposable income to invest.

But the second part of the equation is why rates are being cut. The rate cuts of the past 50 years can essentially be lumped into two buckets – those made out of luxury, and those made of necessity.

In recent history, our rate cuts have been those of necessity, in response to the 2001 recession and the 2008 financial crisis. Looking back further, we have had six necessity rate cut cycles that came in tandem with recessions – 1973, 1974, 1980, 1981, 2001, and 2007. In those instances, the average return for the stock market over the next 12 months was -9.7%.

On the flip side, we have had seven rate cuts made out of “luxury,” that is cuts without a corresponding recession, and the primary aim was to promote growth and get rates back to their neutral level. These cuts came in 1982, 1984, 1987, 1989, 1995, 1998, and 2019. In this, case, the average return for the market over the next 12 months was 17.4%, and markets were up 100% of the time.

We don’t know yet if a recession is around the corner. Going into 2023, the expectation was that rate cuts and high inflation would lead to a recession, but 22 months later that recession has not materialized. If we can avoid a recession, history indicates stocks should do well going forward.

Drilling down a level, rate cuts typically benefit small-cap stocks, as those smaller companies are more likely to rely on loans and variable rate financing to fund operations. Lower interest cost typically leads to greater profitability. While banks and financials like high rates as it increases their interest income, lower rates aren’t necessarily a bad thing. Lower rates often mean lending and refinancing picks up, so while the margin banks are making may start to get squeezed, business may pick up.

Historically rate cuts have also helped stocks in emerging markets, as financing costs and currency pressures ease. However, in an era where tariffs are at the forefront of the political conversation, the election may be more important than rates for emerging markets going forward.

Bonds

Interest rates and bond prices are generally inversely related. When interest rates go up, bond prices tend to go down. We saw a stark example of this in 2022, when the Fed rapidly raised rates from 0.25% to 4.5%, and the Barclays U.S. Aggregate Bond Index declined 13% for the year, its worst year ever.

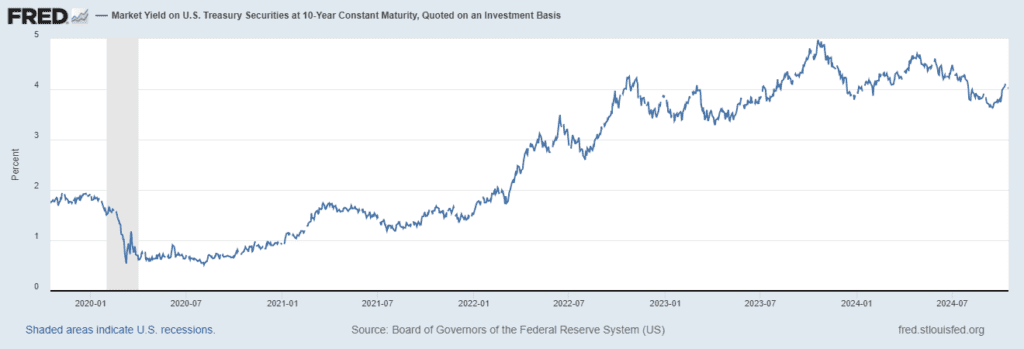

Now we find ourselves on the other side of the equation. When rates go down, bond prices tend to go up. This in process began in the spring, as markets started to price in the potential for rate cuts later in the year. In May, the interest rate on 10-year Treasury bonds stood at 4.6%, and it has steadily declined down to 3.7% in September.

Bond yields do not move in lockstep with Fed interest rate cuts, as other factors like the economy and investor demand have influence as well. But generally, if we are in a prolonged period of rate cuts, we expect bond yield to continue to decline, and bond prices to go up.

In short, this is a positive for bond investors, as they can get appreciation in addition the regular interest paid by their bonds.

Cash

One area that does respond quickly to rates cuts are the cash markets. In fact, yields on savings accounts, CDs, and money market funds have already declined from their peaks. While the interest paid by these accounts is still higher than it was prior to 2023, it may be time to look for a new home for excess cash.

Given the positive outlook for bonds noted above, investors should consider moving cash reserves (those not earmarked for living expenses) into longer term bonds to take advantage of the total return (appreciation + interest) potential.

Mortgage rates

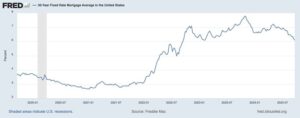

The Fed doesn’t have a say in mortgage rates, but their decisions tend to ripple out across various lending markets. Fixed mortgage rates take Fed rate moves into account along with economic factors like demand and inflation. If anything, they are most closely tied to is the 10-year Treasury yield.

As noted above, the rate on the 10-year declined over the past 4 months, and the 30-year mortgage rate has followed suit. The 30-year mortgage rate moved down from over 7.00% in the spring to 6.08% at the end of the September, the lowest level in more than two years.

In the past the general wisdom was the time to look at refinancing your mortgage was when you could reduce your rate by 1%. However, if you plan to stay in your current home for a while, refinancing down by as little as 0.50% can still make sense in the long-run.

Car Loans, Student Loans, Credit Cards

Car loans often follow the 5-year Treasury rate, though again other factors (market demand, credit score, type of vehicle) are in play as well. Auto loan rates have moved down only modestly, with the rate on a new car loan for those with a credit score above 660 standing around 6.8%.

Credit card rates have fallen as well, though with an average rate north of 20%, carrying a balance on a card should be a last resort.

Federal student loans come with fixed rates, which reset each July 1st, based on the current 10-year Treasury rate. So we have to wait until July 2025 to see the effect on Federal student loan rates. Private loans come with variable rates that may come down, though rates are heavily dependent on your credit score.

Where Do Rates Go From Here?

After each meeting, the Federal Reserve releases something known as the “dot plot.” The dot plot is a chart that shows each member of Federal Reserve’s projection for where rates will be in the future. By averaging together the 19 members’ predictions, we can get a forecast of where rates might be headed.

The current dot plot forecasts the Fed target rate falling to around 4.0% by year-end, followed by another 1.0% worth of cuts in 2025 to get to around 3.0% by the end of next-year.

Sometimes you will hear about a “neutral” rate – one meant neither to stimulate the economy nor to slow it down, but rather to maintain the status quo. The recent consensus has trended toward a neutral rate being 1% above inflation. With inflation currently around 2.5% that would imply 3.5% is a neutral rate. If inflation comes down to 2%, rates may settle around 3%.

Thus, the dot plot forecasts the Fed getting back to a neutral rate by the end of next year.

Source: Bloomberg. FOMC DOT Plot as of 9/18/2024.

There are two mandates the Federal Reserve focuses on – inflation and unemployment. With inflation back to normal levels and seemingly under control, the focus now is on labor. Rate decisions will be driven primarily by unemployment numbers going forward.

The “natural” unemployment rate is thought to be around 4%. Coincidentally the most recent jobs report returned an unemployment rate of 4.2%. If unemployment remains steady, it is reasonable to expect the path above to play out. Should the unemployment rate tick up closer to 5.0%, we would expect swifter rate cuts.

As of now, the base case expectation is for moderate unemployment, stable inflation, and steady rate cuts over the next 12 months. Historically that has been a positive equation for stock and bond investors. Uncertainty is always lurking around the corner, but the current path typically leads towards positive outcomes for investors.

This material is intended for informational/educational purposes only and should not be construed as investment advice, a solicitation, or a recommendation to buy or sell any security or investment product. Please contact your financial professional for more information specific to your situation.

All indices are unmanaged, and investors cannot actually invest directly into an index. Unlike investments, indices do not incur management fees, charges, or expenses. Past performance does not guarantee future results.

Presented by Chris Rivers, CFP®, CRPC®