Metropolis 1927

We like to think we take things at face value.

But it seems that our emotions are not so much reactions to the present as they are guides to the future.

This is one of the conclusions highlighted by psychologist Marty Seligman in a 2017 NY Times article. Seligman notes that we may be far more forward thinking and obsessed with the future the previously thought:

Looking into the future, consciously and unconsciously, is a central function of our large brain, as psychologists and neuroscientists have discovered — rather belatedly, because for the past century most researchers have assumed that we’re prisoners of the past and the present.

In the 20th century, psychological theory explained human behavior as a consequence of each individual’s history, past and present. Freud gave us license to blame everything on our mothers and fathers. But it seems this may not be the way we’re wired, at least not entirely, and it has important implications for our financial lives.

Why is it that we’re obsessed with the future? Are we all just more neurotic than we’d like to admit, caught up in the accelerating pace and pressures of modern life, struggling to adjust to too much change in too short a period of time?

That was the argument made by Alvin & Heidi Toffler in their book Future Shock. Anthropologist Loren Eiseley strikes a similar tone when he writes of

a social environment altering so rapidly with technological change that personal adjustments to it are frequently not viable. The individual either becomes anxious and confused or, what is worse, develops a superficial philosophy intended to carry him over the surface of life with the least possible expenditure of himself. Never before in history has it been literally possible to have been born in one age and to die in another. Many of us are now living in an age quite different from the one into which we were born….Of far greater significance are the social patterns and ethical adjustments which have followed fast upon the alterations in living habits introduced by machines.

In the era of social media and total noise, most of us can probably identify with what Eiseley is saying. But Eiseley wrote that in 1960 and Future Shock came out in 1970, decades before the rise of the internet. So while we can blame technology all we want, it appears our obsession with the future goes back further.

Perhaps much further.

In his recent bestseller, Sapiens: A Brief History of Humankind, Yuvel Noah Harari argues that this behavior is rooted in our transition from hunter/gatherers to farmers some 10,000 years ago.

As humans transitioned to farming and became dependent on seasonal crops, forces beyond our control (temperature, pests, drought, etc.) greatly affected our chance of survival.

Thus man increasingly began to worry about threats that were not real or immediate, but latent in the future:

Peasants were obliged to produce more than they consumed so that they could build up reserves. Without grain in the silo, jars of olive oil in the cellar, cheese in the pantry, and sausages hanging from the rafters, they would starve in bad years. And bad years were bound to come, sooner or later.

Surplus became a key to survival, and we adapted to pursue and acquire more than we needed. This wasn’t greed, it was prudence — those who planned better stood a better chance of surviving.

Old habits die hard.

Thousands of years later, few of us depend directly on farming for our daily survival, but we continue to weigh the future heavily. It set us apart thousands of years ago and landed us at the apex of the food chain.

However, centuries on, we have in one sense outraced our brains. The threats of the Neolithic era have largely been solved, but the software in our heads hasn’t caught up. We overemphasize the dangers that may lay ahead, and discount potential upsides.

Financial columnist Morgan Housel wrote about this in a piece titled The Seduction of Pessimism:

Tell someone everything will be great, and they’re likely to shrug you off…Tell someone you’re in danger, and you have their undivided attention.

Pessimism is often taken more seriously than optimism, which can sound like salesmanship or aloofness.

In short, pessimism can sound practical (even when it’s not) and optimism can sound foolish or fake, even when it is rational and logical.

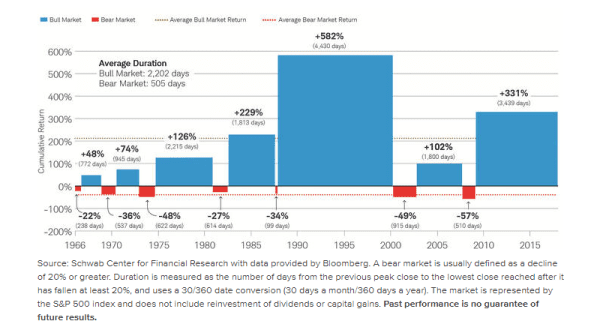

Morgan concludes that within investment markets, “the difference between pessimism and optimism often comes down to time horizon. If a recession or downturn is the end of your show, you should be pessimistic. If it’s a bad commercial during an otherwise great episode, you should be optimistic.”

Recessions and market downturns are just chapters. Most investors have been through at least one of the bad chapters shown in red in the chart above. The problem comes when we take the current chapter and view it as the final act, or the whole story. Even armed with the context provided by the chart above, it is difficult to remain stoic while watching your portfolio decline.

At the time of the 2008 crisis, the iPhone was in its infancy, with 13 million phones worldwide, (versus 217 million iPhones sold in 2017.) Last time the market crashed, most of us were using one of these.

The next bear market will come in a time of unprecedented connectivity and interaction, thanks to the rise of smartphones, social media, streaming video, and instant account access. It’s reasonable to assume then that the next bear market may not be of the “slow and steady” variety.

When the market drops, our Neolithic software will kick in. It will be difficult to convince ourselves that — when bombarded by news reports, tweets, shared articles from friends, and phone alerts — the current decline too shall pass, just as previous declines have.

It will be easy to attribute the day’s or week’s decline to some bit of recent information — a bad jobs report, higher inflation, or increasing oil prices. But this too is a trap, one that psychologists call the “narrative fallacy.”

Our brains evolved to piece together explanations after the fact, with nice and tidy causes and effects. Novelist Cormac McCarthy said it more eloquently when he wrote

…the order in creation which you see is that which you have put there, like a string in a maze, so that you shall not lose your way.

Often during the crisis of 2008–2009, the evening news attempted to lay the string in the maze, attributing the market drop to a bad economic report released earlier that day.

But economic reports are typically released at 8:30 AM or 10:00 AM, depending on the report. A closer look at many of the days when the market dropped showed large declines and the heaviest trading in the 3:30 PM to 4:00 PM window.

Are we supposed to believe that millions of market participants collectively contemplated the economic report for 5 hours, and then decided to panic? And lest we forget, up to 90% of the trading done on the market each day is driven by computers and algorithms, not a do-it-yourself investor analyzing the latest GDP report.

If we accept that we worry about the future, overvalue reports of gloom and doom, and see patterns that may not exist, what can we do about it?

Planning just may be our best tool.

Going back to Marty Seligman in the New York Times:

When making plans, [people] reported higher levels of happiness and lower levels of stress than at other times, presumably because planning turns a chaotic mass of concerns into an organized sequence. Although they sometimes feared what might go wrong, on average there were twice as many thoughts of what they hoped would happen.

The antidote then, at least when it comes to our wallets and our portfolios, is a comprehensive financial plan. One that looks at what you’re earning versus what you’re spending each year, and projects your path decades into retirement. A plan that covers taxes, investments, insurance, education funding, Social Security, estate planning, and more.

The planning process forces us to face our fears, just as our ancestors did 10,000 years ago. The backbone of a true financial planning process is a discussion about where you’ve come from, where’d you like to go, and what keeps you up at night. The next bear market may be one of those things, but a plan can reduce a mountain of worry to rubble.

Further Reading:

The Seduction of Pessimism by Morgan Housel

We Aren’t Built To Live in the Moment, by Marty Seligman & John Tierney, New York Times

Sapiens: A Brief History of Humankind by Yuvel Noah Harari

The Firmament of Time by Loren Eiseley

Blood Meridian by Cormac McCarthy

A Bear-Market Tool Kit, Charles Schwab

Machines Are Driving Wall Street’s Wild Ride, Not Humans, CNNMoney