As a decade of low interest rates came to a rapid end, bonds did not act like themselves in 2022, which marked the first year in a generation that bonds fell alongside stocks. To wit, the Bloomberg U.S. Aggregate Bond Index’s total return was good for -13.01% in this period.

The declines came as the Federal Reserve (Fed) embarked on one of its most aggressive interest rate hiking campaigns in history to combat inflation, raising its benchmark rate 5.25% in less than a year and a half. Bond prices move opposite interest rates, so when interest rates rise, bond prices fall. That’s because new bonds are issued at higher interest rates, making previously issued bonds less valuable. It was a good reminder to investors that bond returns are driven both by its coupon (how much interest a bond pays) and price, but the price return component is key in a rising interest rate environment, particularly since starting yields were so low.

The start of bonds’ comeback?

After a miserable 2022, bonds staged a remarkable comeback at the end of last year. Bond yields peaked in mid-October, then fell, which caused prices to increase. These gains mark a major reversal as investors went from thinking the Fed might need to hike rates even further to betting that the central bank is finished and might even lower rates sooner. As a result, the Bloomberg U.S. Aggregate Bond Index seemed to be flirting with a negative return for the third consecutive year, but finished with a positive return of 5.53%.

The longer-term outlook for bonds has improved

The good news is that even after a sharp rally in late 2023, bond yields still look more attractive than they have in a long time, currently around 4-5% compared to 2% or lower for much of the last decade. This is significant, as most of a bond’s return over time comes from its yield. More, the odds are likely more in favor of interest rates falling than increasing as current Fed guidance calls for approximately three cuts of 0.25% each in 2024 and four additional cuts in 2025.

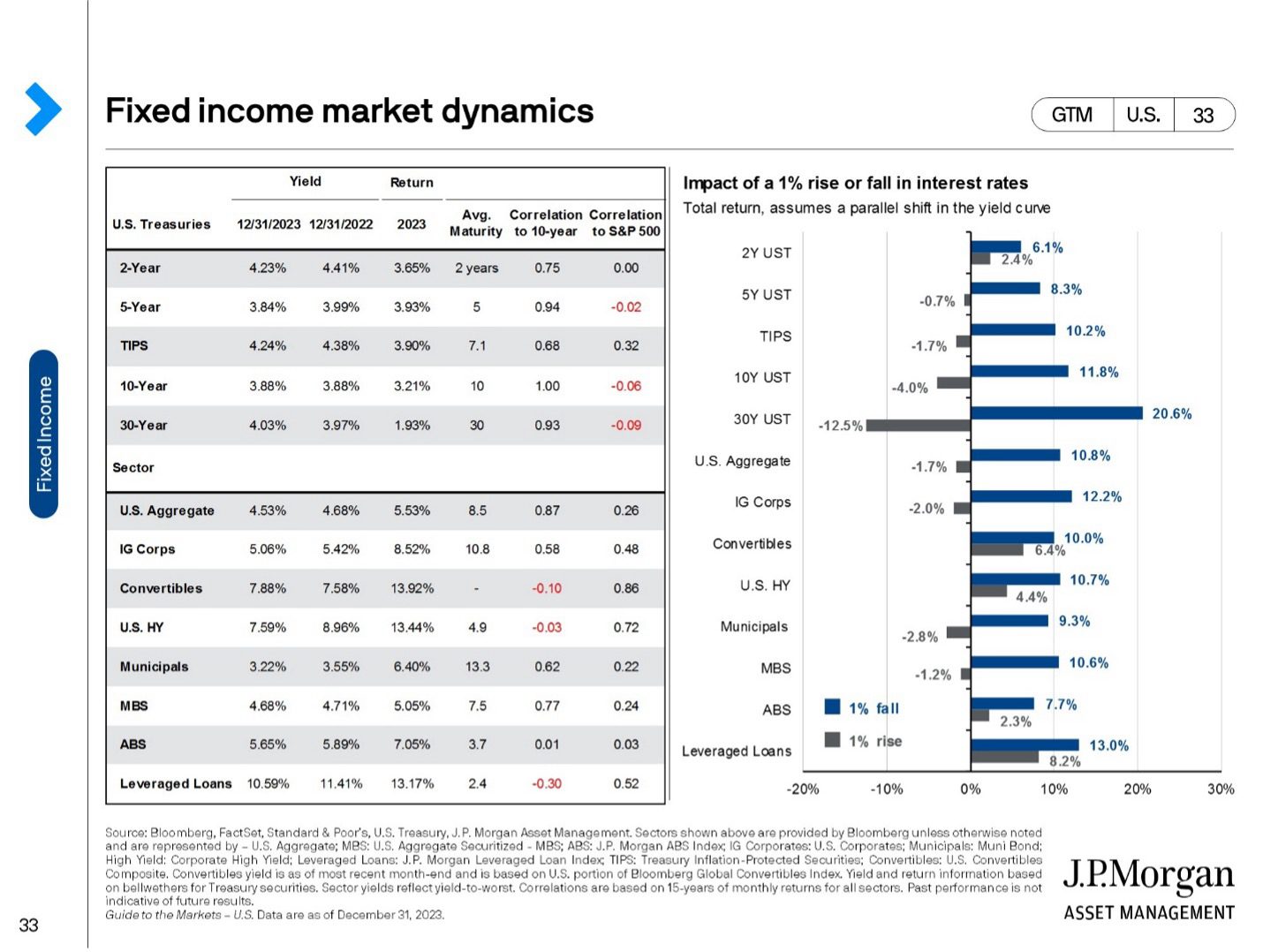

Why is this important? It could provide a nice tailwind to bond investors going forward. The right-hand side of the chart below shows the impact of a 1% rise or fall in interest rates across various parts of the fixed-income market. If economic growth weakens as some economists forecast, it is likely the Fed could accelerate interest rate cuts which would further boost bond returns.

Why not just sit on cash?

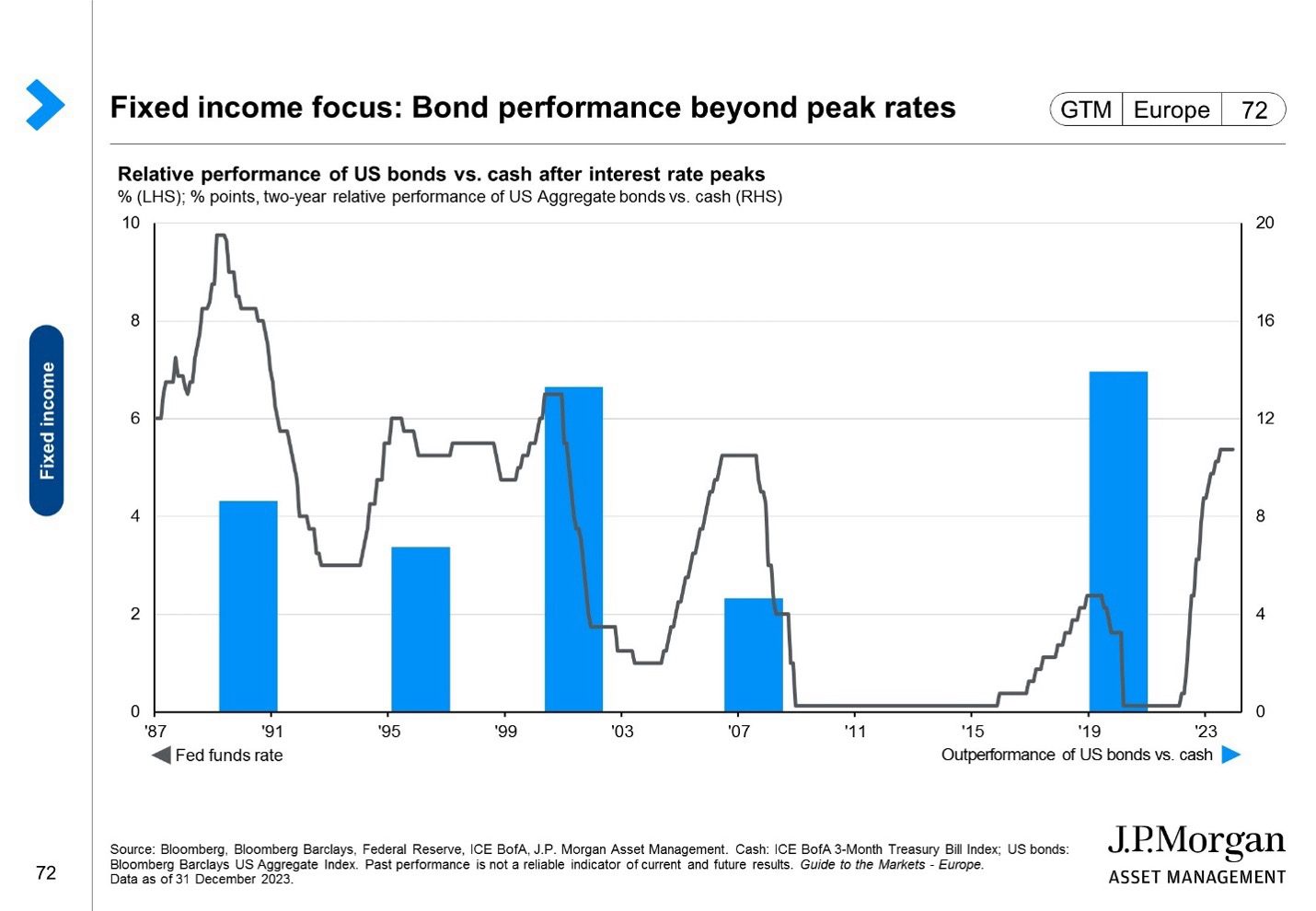

Investors may be sitting n cash given its attractive higher yield, but may not realize that cash yields are likely to fall quickly as the Fed cuts rates. While cash yields are around 5% annualized today, the actual return for an investor holding through the Fed cuts in 2024 will likely be less than that. Also, cash loses out on the price appreciation that occurs in bonds when interest rates fall. The chart below illustrates this by showing the performance of fixed-income relative to cash following a peak in US interest rates. The line plots interest rates over time while the blue bars show the subsequent two-year performance of the US Aggregate bond index relative to cash rates from the peak in each hiking cycle. As you can see, bonds outperformed cash following the last five peaks in interest rates.

In Conclusion

There is no certainty in today’s market environment, but the prospects for bonds look brighter than they have in a long time. After a long slump, bonds may finally be poised to resume their role of providing income and diversification in investors’ portfolios.

Bonds are subject to availability and market conditions; some have call features that may affect income. Bond prices and yields are inversely related: when the price goes up, the yield goes down, and vice versa. Market risk is a consideration if sold or redeemed prior to maturity.