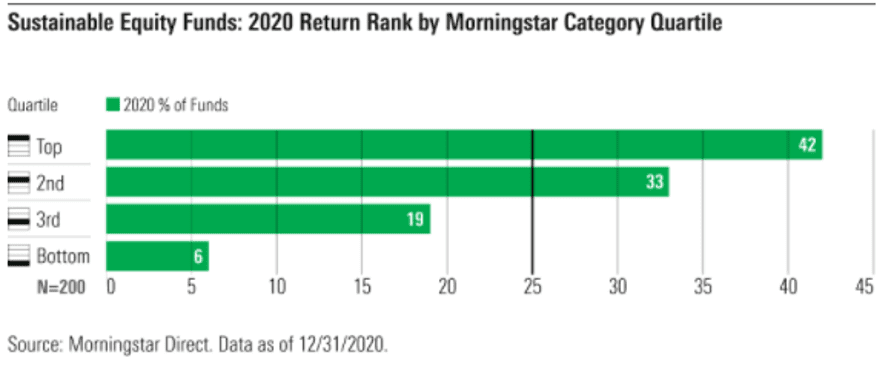

As the dust settles on a year that was like no other, we can now look back at 2020 and see where we stand today. Although the pandemic highlighted a rather terrible year overall, it wasn’t bad for investing and, relatively speaking, it was another good year for socially responsible investments (SRI). Looking at equity investments specifically, three out of four sustainable equity funds beat their Morningstar Category average in 2020, and far more sustainable funds finished the year with performance that ranked in the top quartile (42%) than in the bottom quartile (6%).

MSCI Inc. reports that in 2020 their World SRI Index, which includes large and mid-cap stocks across 23 developed countries with outstanding environmental, social, and governance (ESG) ratings, returned 20.5% which topped the 16.5% gain for the non-SRI compliment MSCI World Index. On the fixed income side, the Barclays MSCI ESG Focus US Aggregate Bond Index finished the year up 7.7% compared to the 7.5% return for the non-ESG focused Aggregate Bond Index.

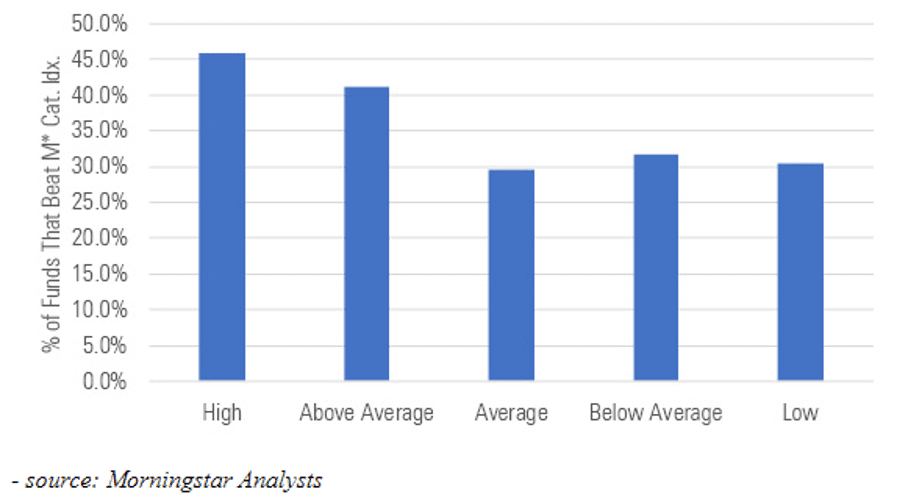

As with any asset class, not all investments are the same and certainly will not have the same outcomes. Morningstar Sustainability Ratings, also known as “globe” ratings, are assigned to funds based on how much ESG risk their holdings have, with those funds who court less ESG risk receiving higher ratings (e.g. four or five globes). As shown in Exhibit 1, they found that funds with higher ratings (i.e., less ESG risk) beat their traditional style-specific index more often than funds with lower ESG ratings. As shown, a larger percentage (above 40%) of funds rated “high” or “above average” (meaning lower ESG risk) outperformed their benchmark as compared to only 30% of funds rated “low.”

Exhibit 1: Percentage of ESG-Rated Funds That Beat Their Index in 2020, by Rating

Will asset growth & out performance continue for ESG/SRI going forward?

We certainly think it can, and there are multiple reasons to believe that it will. Despite serious concerns ESG investing trends would be derailed when President Trump took office four years ago, his rhetoric and regulatory changes were unable to slow the growth of socially conscious investing. Just looking at the past two years, US assets using ESG investing strategies increased 42% to $17 trillion in 2020 up from $12 trillion at the start of 2018, according to the United States Forum for Sustainable and Responsible Investment (US SIF) biennial report released on November 16th. Therefore, ESG has generally outperformed and proven it can continue amassing assets, despite headwinds.

Under President Biden’s new administration, we are already beginning to see positive signs (e.g. rejoining The Paris Agreement) that his policies will likely support ESG investing. Many of his proposed cabinet choices provide further evidence of that as well. There is also the belief that the SEC and Labor Department will roll back Trump administration rules limiting the use of ESG funds in retirement plans and the ability of ESG investors to participate in the shareholder resolution and proxy voting process. The SEC could also move to require public companies to include climate-related financial risks and greenhouse gas emissions in their financial reporting moving forward.

If there is a silver lining to the 2020 cloud, it’s the fact that many social justice and sustainability issues were brought to the forefront. As more investors, both retail and institutional, look to make a positive impact on these issues through their investments, asset growth for ESG/SRI will likely continue. With a number of factors indicating a bright future for ESG/SRI, it also appears that sustainable investors should continue to benefit with a presidential administration that is more supportive and focused on making socially conscious investing accessible to the masses.