While you might already be invested in an employer-sponsored plan like a 401(k), an Individual Retirement Account (IRA) allows you to save for your retirement on the side, and potentially save on taxes. However, there are two different types of IRAs: traditional and Roth that each have different rules and benefits.

IRA Basics

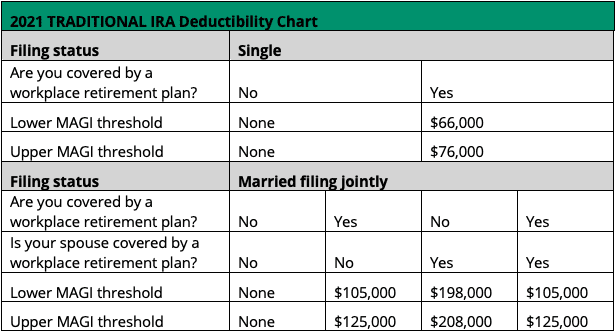

In a traditional IRA, you can contribute up to $6,000 or $7,000 if you are 50 or older. You must have enough “earned income” (wages, salaries, tips, bonuses, commissions, and self-employment income) to cover your contribution to an IRA. If your earned income for the year is less than the contribution limit, you can only contribute up to your earned income. For example, if you earned $3,000, you could contribute a maximum of $3,000. Your money grows tax-deferred, but withdrawals are taxed as current income after age 59½. Additionally, the traditional IRA may offer an upfront tax deduction. This depends on your modified adjusted gross income (MAGI), and whether you or your spouse is covered by a retirement plan at work as noted in the chart below.

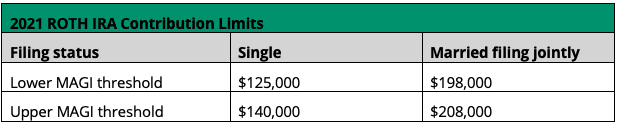

With a Roth IRA the contribution limits are the same as the traditional IRA, your money grows tax-free, and you can generally make tax- and penalty-free withdrawals after age 59½. Unlike a traditional IRA there is no upfront tax break, and you can only make contributions if you are below certain income levels.

Is your income too high to allow you to make a Roth IRA contribution? Don’t worry as there are still ways to set aside money away into this tax-free account. If your company’s retirement plan offers a Roth option, there are no income limits on contributions through the plan. For those with money already in a traditional IRA, a Roth conversion is an option. For those without any IRA assets, a backdoor Roth contribution is another way to get around the income limits.

Pay taxes now or pay later?

When asked if they would like to pay taxes now or at some point in the future, most people would tend to defer the payments. While that is sound thinking, it omits one key element: what the tax rate in the future might be once the money is withdrawn. The general rule of thumb is that if you expect a higher tax rate in the future, then owning a Roth IRA is a better option. But what if your tax rate is the same now as it will be when you start taking withdrawals? Let’s look at a hypothetical example to find out.

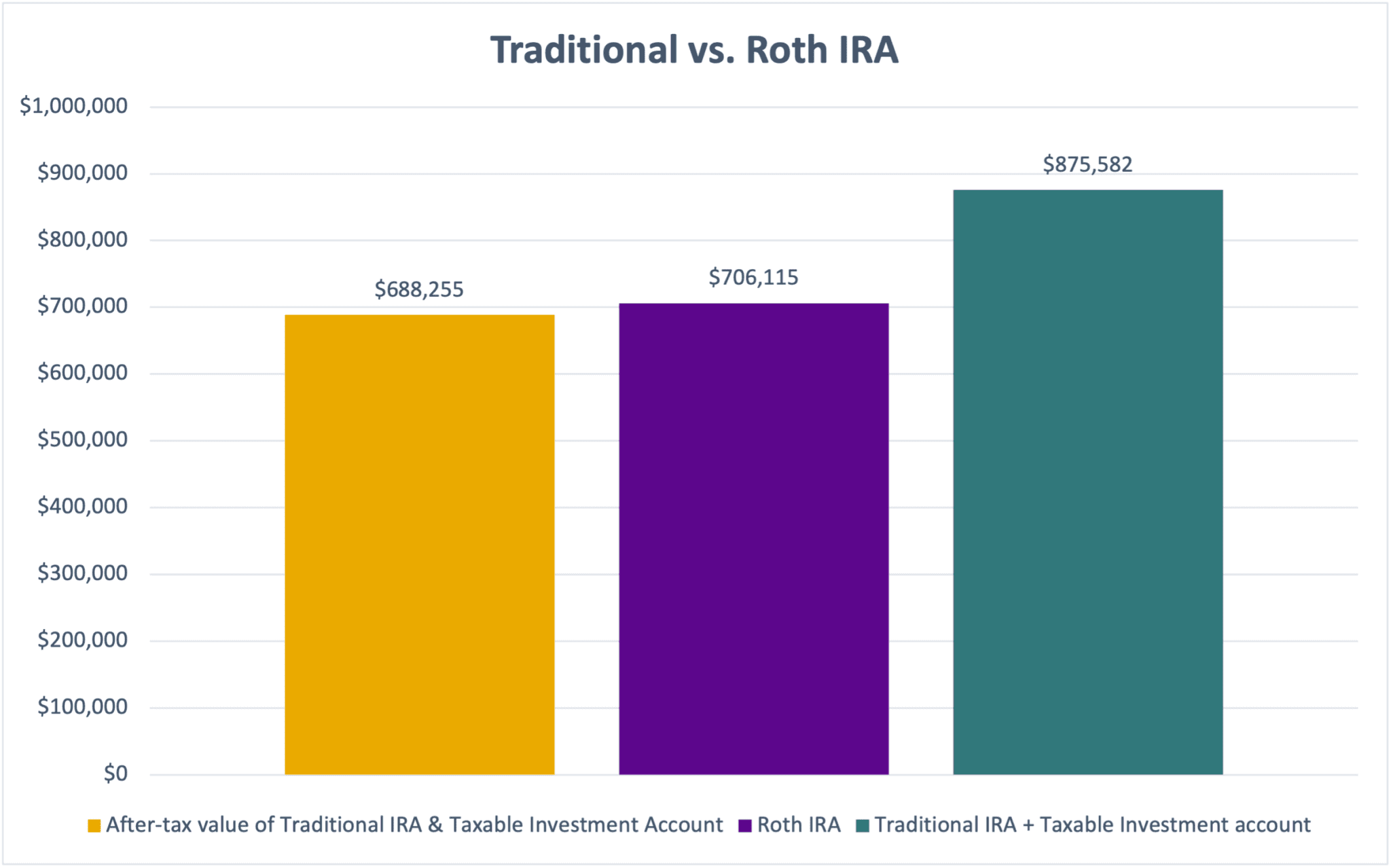

Assumptions:

- A 30-year-old makes annual $6,000 contributions to a traditional (deductible) IRA or a Roth IRA for 25 years

- Current and future income tax rate is 24%

- Tax savings generated by the traditional (deductible) IRA contributions are invested in a taxable investment account

- Taxable investment account’s gains are taxed at 15%

- Rate of return on all accounts is 6%

As noted in the chart below, the total value of the traditional IRA and tax investment account is worth far more than the Roth IRA after 25 years. However, the after-tax value of these two accounts is worth less than the IRA! What this implies is that even if your tax rate is the same or lower in retirement, the Roth IRA may still be a better option than the rule of thumb suggests.

This is a hypothetical example and is for illustrative purposes only. No specific investments were used in this example. Actual results will vary. Past performance does not guarantee future results.

This is a hypothetical example and is for illustrative purposes only. No specific investments were used in this example. Actual results will vary. Past performance does not guarantee future results.

Roth IRA’s additional advantages

In addition to generating a potentially larger after-tax benefit during retirement, below are five more notable advantages the Roth IRA offers over a traditional IRA account.

- Tax-free withdrawals at any time: With a Roth IRA, you can withdraw your contributions at any time, for any reason, without tax or penalty. Earnings can be withdrawn tax-free once you are at least 59 ½ years old and it’s been at least five years since you first contributed to a Roth IRA.

- Say goodbye to Required Minimum Distributions (RMDs): Roth IRA account holders are free to let all their money stay put for as long as they’re alive, which gives them much more flexibility on when and how to take withdrawals. This also allows the investments to grow tax-free for longer and can help you avoid selling assets at a bad time.

- Avoid triggering additional taxes in retirement: With qualified withdrawals from a Roth there is no taxable income, so there’s no chance of distributions increasing your tax on your social security benefits, increasing your Medicare premiums, or triggering the Medicare surtax of 3.8% on investment income.

- “Lock-in” current tax rates –Tax rates have fallen dramatically over the past 60 years. The highest marginal tax bracket in 1960 was 91% and is now down to 37% in 2021. By paying taxes now this removes the uncertainty of what future tax rates might be.

- Estate planning considerations for beneficiaries: For most non-spousal beneficiaries, both traditional and Roth IRAs are required to have the entire account to be distributed by December 31 of the tenth year following the year of death. For those with sizable IRAs or beneficiaries in higher tax brackets, this can create a significant tax headache for them. Leaving them a Roth allows them to receive an asset without an embedded tax liability.

So, what’s the verdict, traditional or Roth IRA?

It’s clear the upfront tax benefit of a traditional IRA isn’t as great as it first appears in certain circumstances. However, that doesn’t mean a Roth is the right answer since everyone’s situation is unique. It’s also important to note that it isn’t a binary choice, you can split your contribution between a Roth and traditional IRA any way you like up to the total maximum allowable amount (the same goes for retirement plans like 401ks that offer a Roth option). Just like we advocate that all investors have a diversified portfolio, we think it’s important to have a third ‘tax-free” bucket of savings in retirement. If the decision all feels a bit overwhelming, feel free to reach out to us to help you set up a plan and invest for your future.