It’s a scary time for anyone who recently retired and for those about to. Stocks (as measured by the S&P 500 Index), for example, have dropped more than 20% this year. Despite the negative headlines, this is a regular occurrence, as a 20% or greater decline is expected about every seven years. The big challenge in 2022 has been bonds, which have also dropped sharply. Traditionally, bonds served as a buffer when stocks declined, but the Bloomberg U.S. Aggregate Bond Index is also down over 15% this year. Bond prices moved lower in response to the Federal Reserve raising its benchmark interest rate. This could be a serious concern for retirees looking to rely on their portfolio for income in the coming years. High inflation also means retirees may need to draw more from their portfolios to cover their expenses.

Why the downturn matters for retirees

Retirees are most vulnerable to market shocks in the early months and years of retirement. This is due to “sequence of returns” risk. Someone who withdraws money early in retirement from a portfolio that’s declining in value is at greater risk of depleting their nest egg too soon, relative to a retiree who suffers a market downturn years later. They may need to sell more of their investments to generate income, leaving less to grow when things rebound.

However, there are steps retirees — and those planning to retire soon — can take to protect their nest egg.

- Adjust your spending – While retirees can’t control the returns of the stock and bond market, they can control their spending. They could reduce their spending, thereby reducing their withdrawals from the portfolio. Does it mean you can’t take a fun cruise or vacation? Not necessarily, but you should carefully think about the potential tradeoffs, as spending more now might limit your future.

- Choose carefully where to take your withdrawals – You don’t want to be selling stocks or bonds in this environment if you can afford not to. Instead, consider taking withdrawals from a cash bucket, which allows you to keep your other assets invested and fully prepared to participate in the recovery. If you don’t have enough cash on hand, consider pulling from areas that haven’t been hit as hard as others, such as short- or intermediate-term bond funds.

- Work longer – Depending on how far the markets fall and how their portfolio is positioned, pre-retirees may need to consider working longer, if possible. Or rather than stopping work entirely, one could reduce their hours to put less pressure on their nest egg.

- Diversify beyond traditional stocks and bonds – Alternative investments can help diversify the portfolio and help lower overall risk. Because these alternatives tend to have lower correlations to traditional investments, they may differ from those of traditional investments. Examples would include real estate, managed futures, commodities, hedge funds, etc.

“Past performance does not guarantee future results,” but it does tell us something

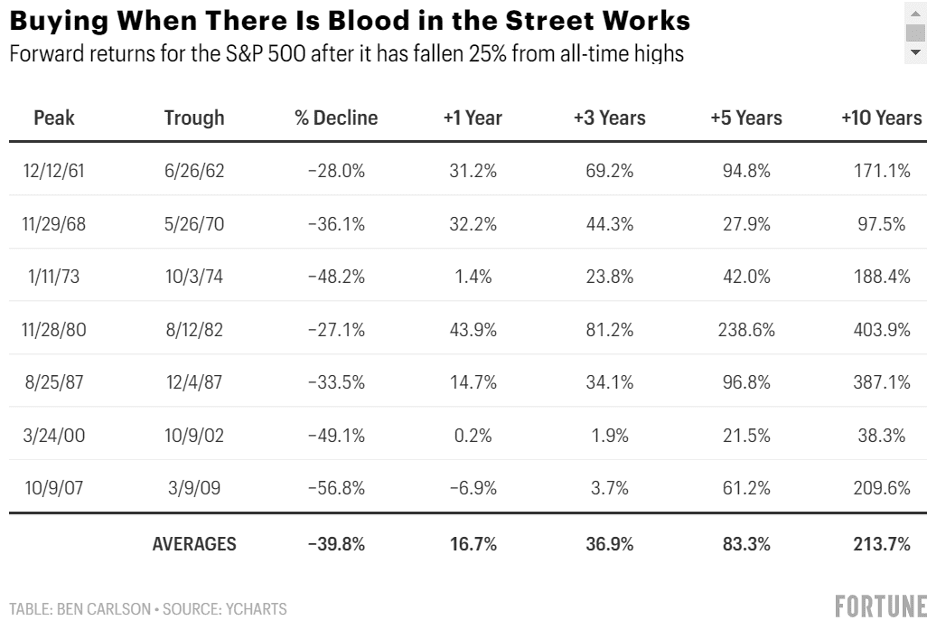

The statement above is embedded in the disclosure pages of nearly every financial instrument in the U.S. The reality is that if an investment has done especially poorly in the recent past, because of its new, lower pricing, it may have a greater chance of doing well in the future. The chart below from an article by Ben Carlson shows how the S&P 500 has performed after it declined 25% going back to 1950:

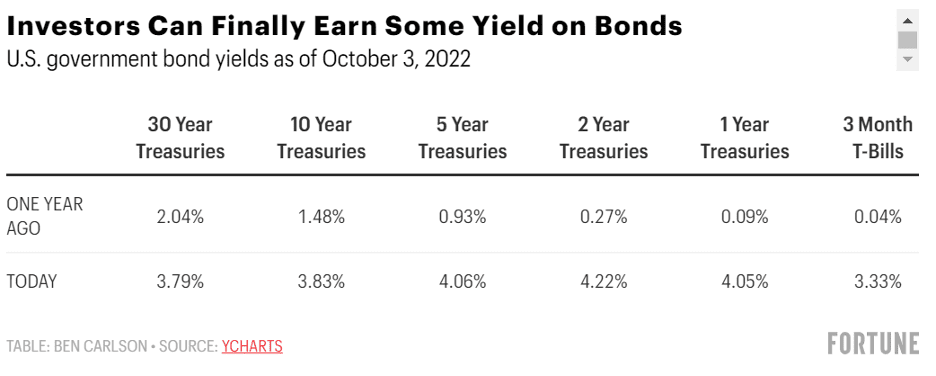

But what about bonds? The reason bond returns have been so dreadful this year is because interest rates are higher, and the starting yields were so low. It was really the worst combination you could hope for when it comes to fixed income. But now that those yields are so much higher, investors have a much bigger margin of safety should rates continue to rise. And the best part for retirees is that short-term bonds, such as one- and two-year Treasuries, now have higher yields than long-term bonds (see chart below). This is a good thing because, all else equal, the shorter the duration (measure of a bond’s sensitivity to interest rate changes) in the bond or bond fund, the lower the volatility in price when interest rates move. There is a higher margin of safety for bonds when rates are at 4% than when they were closer to 0%.

It took some pain to get here, but the outlook for future returns is looking better for retirees. As always, things could get worse before they get better, but the good news is that there are ways to prepare for and combat these challenges.