In the introduction to his 2016 book “The Attention Merchants,” Tim Wu writes:

As William James observed, we must reflect that, when we reach the end of our days, our life experience will equal what we have paid attention to, whether by choice or default. We are at risk, without quite fully realizing it, of living lives that are less our own than we imagine.

Although James made his statement in the late 19th century, it’s not hard to see how it applies to the digital age. Writer David Perell has referred to it as the “Never-Ending Now,” with social media and 24-hour cable news feeds that push us to focus on what just happened, search for what’s next, and encourage us to lose site of the forest for the trees.

“We’re trapped in a Never-Ending Now,” Perell writes, “blind to our place in history, engulfed in the present moment, overwhelmed by the slightest breeze of chaos.” There is a growing body of literature examining the effects this myopia is having on our happiness, but what about our financial well-being?

In a 2011 speech, Andrew Haldane of the Bank of England noted that our brains are adapting to the increasing volume of information by shortening our attentions spans. Haldane found that investment choice, like other life choices (marriage, jobs), is being re-tuned to a shorter wavelength. Greater returns are expected in shorter time frames than before, and simple day-to-day market fluctuation is often interpreted as a signal of an impending crisis.

In a recent article in the Wall Street Journal Dr. Shlomo Benartzi, professor of behavioral economics at UCLA, wrote about the impact of information overload on our financial lives.

Benartzi notes that prior to rise of the internet, information on markets was scarce. One of the primary barriers to successful investing was a lack of access to the proper information required to make informed decisions. In fact, the fortunes of many of the infamous “robber barons” of the late 1800’s were built on the possession of knowledge about markets and companies that the public at large did not have.

A century later, we find ourselves in almost the exact opposite predicament. Writer David Foster Wallace called it the era of “Total Noise,”

a kind of Total Noise that’s also the sound of our U.S. culture right now, a culture and volume of info and spin and rhetoric and context that I know I’m not alone in finding too much to even absorb, much less to try to make sense of or organize into any kind of…value. Such basic absorption, organization, and triage used to be what was required of an educated adult, a.k.a. an informed citizen — at least that’s what I got taught. Suffice it here to say that the requirements now seem different.

As the saying goes, if you’re not paying for the product, you are the product. The more a user engages with a platform or channel, the more data the provider can collect about the user, and the more valuable they are to that platform’s advertisers. As a result, the purpose of the content pushed to us 24/7 is not to inform, but to engage, to track, and to monetize.

In the era of total noise, successful financial decision making requires a combination of filtering this flood of information, reflecting on it, and placing it in the proper context. This sort of triage, reflection, and analysis can be easy to bypass when we focus on the latest alert, tweet, text, or newsflash from the phone in our pockets.

In fact, Bernatzi writes that research “shows that people tend to perform worse on a test of financial literacy when given the questions on a mobile device, at least compared with those subjects taking the same test on paper.”

One likely explanation involves the tendency of people to think and read faster on their smartphones, as we continually scroll down the screen for more stimulation. And the news gets even worse. Recent work by Adrian Ward, Kristen Duke, Ayelet Gneezy and Maarten Bos shows that just having your smartphone next to you — even if it isn’t turned on — can diminish your cognitive capacity.

Distraction is not a new phenomenon, and certainly not unique to the internet era. In the Odyssey, one our oldest stories, Odysseus famously has himself tied to the mast of his ship as he sails past the Sirens so that he will not be overcome with distraction and veer off course.

While lashing ourselves to the mast isn’t an option, there are a few things Benartzi recommends to put ourselves in a position to make better financial decisions and stay on course, among them:

- Put the phone away — place your phone away when it’s time to make decisions that take more require some consideration

- Avoid multitasking — there is now a wealth of research demonstrating the human brain cannot effectively handle multitasking, and that all tasks suffer when we attempt to juggle multiple burdens at once

- Pick the right time of day — hard choices are best made during periods when we have the proper attention to devote to the task. For some mornings are quiet and reflective, a perfect time make complex decisions. For others, they are hectic and harried, the worst possible time to consider and reflect

- Focus on the relevant information, not the most available — focus on investment performance that matches your time horizon, and place data in the proper historical context

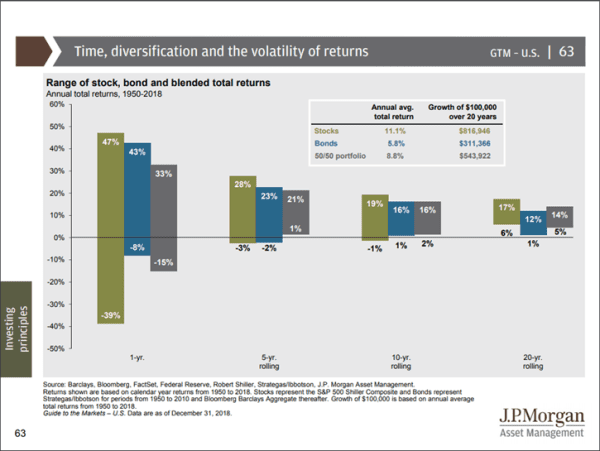

Market returns in 2018 offer a good example of the last bullet point. Following December’s swoon, the S&P 500 ended the year down 4.4%, while international markets dropped further. As the chart below from J.P. Morgan illustrates, the range of outcomes over any one-year period is large, with the S&P 500 posting returns of between -39% and +47% since 1950. Over longer time periods (5, 10, and 20 years), the ranges are much tighter, and the historical returns have been overwhelmingly positive.

Viewed in this context, investment fluctuation over a given year in a long-term portfolio becomes less fearsome. With money earmarked for short-term expenses set aside in cash, the rest of a portfolio may be geared towards ten and twenty-year growth, and daily market fluctuations become the concern of traders and headline writers, not long-term investors.

In our office, we make a concerted effort to adjust continually the way we work to improve client outcomes. To the extent possible we schedule meetings during designated times each day, block off time for specific topics or projects, and provide a charging station in our conference rooms to occupy phones for our clients during meetings.

However, perhaps the most effective way to short-circuit the information overload when it comes to markets and investing is to refer back to your financial plan. Your financial plan is the lens through which all spending and investing decisions should be made, and it provides the proper context to understand to what extent market moves should matter to you.

Every time our attention is captured, our awareness, and perhaps something more, has been appropriated without our consent. A comprehensive financial plan provides the lens through which we can place market news in context, make informed decisions, and navigate the era of total financial noise.

Further Reading:

The High Financial Price of Our Short Attention Spans, Wall Street Journal, 10/21/2018

The Never-Ending Now, perell.com, 11/31/18

The Short Long, Andrew Haldane, May 2011

The Attention Merchants by Tim Wu

Information: A History, A Theory, A Flood by James Gleick

The Information Diet: A Case for Conscious Consumption by Clay Johnson

Ten Arguments for Deleting Your Social Media Accounts Right Now by Jaron Lanier