Investing is a powerful tool that can help build your wealth and secure your financial future. However, there are plenty of pitfalls out there that could hurt your progress. Simply being aware of these pitfalls can improve your chances of success.

- Delaying investing

Getting started investing is probably the hardest part, as some people don’t know where to begin. However, the earlier you start off saving, the better off you’ll be due to the magic of compounding returns. Let’s look at an example:

- Andrea saves $5,000 per year for retirement starting at the age of 25 until she retires at age 65.

- Brian gets a later start than Andrea and does not start saving for his retirement until he is 35. He contributes the same $5,000 per year for the next 30 years, until he retires at age 65.

- Assuming a 7% annual return for both of them, Brian’s account balance will only be $472,304 while Andrea’s will be worth $998,176.

Andrea saved only $50,000 more than Brian, yet her account is more than double. Just for Brian to catch up he would have to more than double his annual $5,000 investment!

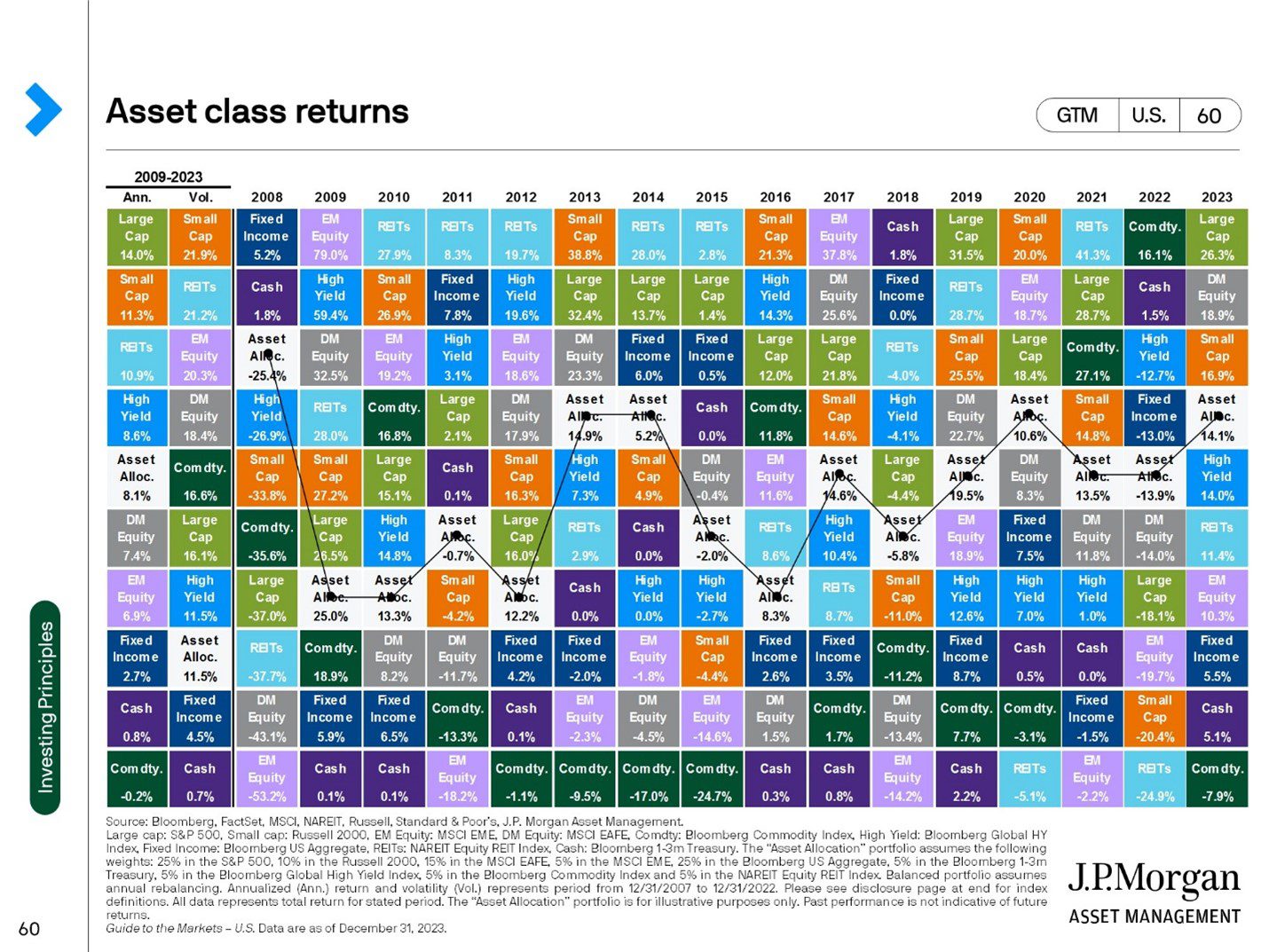

- Chasing performance

The warning “past performance is not a guarantee of future results” appears on nearly all investment materials. Yet, investors are infamous for investing in something simply because it did well in the past. It’s like driving using only your rearview mirror — we know what happened in the past, but we really don’t know what’s coming down the road. An interesting exercise is to cover the chart below and try to guess which asset class will be the best or worst performers each year. Hard, isn’t it?

- Not Being Diversified

Having your portfolio concentrated in a single stock is just like having all your eggs in one basket. If that stock underperforms or the firm goes bankrupt, it could cripple your portfolio and your financial future. This is why diversification is key, for it helps reduce this risk and can limit losses by investing across multiple types of investments. As you can see in the chart above, a hypothetical diversified portfolio will never be at the top, but then it’s never at the bottom, providing a much smoother experience.

- Letting emotions drive your decisions

Fear and greed are powerful motivators that can cause us to make decisions that may hurt investment returns. We may see a stock skyrocketing and want to get in on the action because we don’t want to miss out, only to see it crash. On the other hand, markets may be in a downturn, and you decide to stop investing, or, worse, sell out entirely. Remember, stock returns can vary greatly over short time periods, but over the long term, can reward patient investors.

- Trying to Time the Market

Selling all of your stock before the market falls, and buying them back is a brilliant strategy, but it’s nearly impossible to pull off on a consistent basis. Why? Because missing the down days means you may be missing out on the up days as noted in the chart below. Your investment results are going to be far more influenced by your asset allocation (how much you own in stocks, bonds, cash, etc.) than by when you make the investments.

- Following advice from the news or social media

Getting stock tips or information from the wrong source is another common and costly investing mistake. Often, you only hear about an investment from these sources only after it has already performed well (see mistake #2). The takeaway here is don’t take investment advice from someone that doesn’t know your personal financial situation, and make sure to do your own research or consult with a financial advisor to see if it’s appropriate for your situation.

How to combat these mistakes

- Automate your savings

Automating tasks can help make life easier and the same could be said for investing. If you make your investment savings automatic, you tend to keep on track no matter what else is going on in your life or in the world around you.

- Set aside a play account

Have the itch to make market calls or dabble in the latest stock idea? Set aside a portion of your money into a separate investment account. Ideally, you should limit this to no more than 10% of your portfolio and it should be money that you could afford to hit zero.

- Create a plan with goals

If you are going on a journey to a new destination, you are likely going to need a plan to ensure that you don’t get lost along the way. Be clear on what you are trying to achieve. For example, are you saving for a deposit on a house? Or are you saving for retirement? It can help keep you on the correct route to make sure you don’t drive off the road! Also, make sure to write it down, humans are far more likely to stick with a plan if it’s on the record somewhere.

- Work with an advisor

It sounds self-serving, but yes, working with a financial advisor can help you prevent and limit these mistakes. A financial advisor can help determine where you are in the investment life cycle, what your goals are, and how much you need to invest to get there.

Presented by Carl Holubowich