Context, History, and What to Watch

The financial press loves a good catchphrase. Every market cycle seems to produce its own memorable moniker, and today we are in the era of the “Magnificent Seven.”

This small yet mighty group of companies has driven an outsized share of market returns recently, and its growing weight in major indices has raised questions about whether the market is out of balance.

The Mag 7 are almost all household names – Apple, Microsoft, Amazon, Alphabet (Google), Nvidia, Meta (Facebook), and Tesla. As of the beginning of the year, these seven stocks made up close to 35% of the S&P 500 Index. If we add in JP Morgan, Broadcom, and Berkshire Hathaway, we see the top 10 stocks make up almost 40% of the index, with 490 stocks making up the remaining 60%.

Market concentration is neither new nor unusual, though it has risen well above levels seen in previous years. Following three consecutive years of strong market returns, it is a good time to step back and take stock of what the market looks like in 2026.

What We Mean by “Market Concentration”

Market concentration is simply a measure of how much of the total market value is accounted for by a relatively small number of companies.

In a market‑capitalization‑weighted index like the S&P 500, the index is not made up of 500 equal sized (0.2%) slices, one for each company. Instead, each company is weighted by its market cap – the number of shares outstanding multiplied by the share price.

For example, as of April 2026, Amazon had 10.7 billion shares outstanding, and a share price of $209.78 per share. 10 billion multiplied by $209.78 gives them a market cap of $2.2 trillion. As a result, Amazon makes up 3.8% of the S&P 500 Index.

Market concentration rises naturally in periods when the largest companies outperform the rest of the market. We’ve seen this acutely over the past few years, as the market cap of the largest tech giants swelled, with the 10 largest companies growing from 22% of the S&P 500 in 2020 to just shy of 40% today.

A Recurring Feature of Markets

One of the most useful antidotes to anxiety about market structure is history. Over the past two centuries, U.S. equity markets have repeatedly cycled between periods of broad participation among many stocks and periods of narrow leadership where a few companies outperformed the rest. Each era produces its own mega firms, often tied to major economic or technological shifts.

Banks dominated early American markets. Railroads followed. Industrial conglomerates, energy companies, and consumer giants each had their turn. In more recent memory, we have seen the shift from energy to big banks and big pharma to big tech.

Markets have a long history of elevating certain groups of stocks to near‑mythic status. The “Nifty Fifty” of the 1960s is one such example—a period when a concentrated group of industry leaders captured disproportionate attention and returns. These eras don’t end abruptly, but they do tend to give way over time, as competition increases and leadership broadens.

Elevated, But Not Unprecedented

By recent standards, current market concentration is high. The largest companies now represent a materially larger share of the S&P 500 than they did a decade ago.

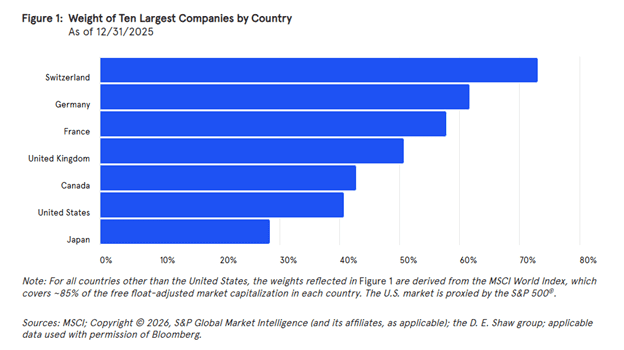

If we zoom out and take a global perspective, we see that many global equity markets are more concentrated than the U.S., not because they are riskier, but because they have fewer large public companies. Even after the recent rise, the U.S. remains one of the more diversified major equity markets globally.

Part of the interest in the current situation comes less from the level of concentration than the speed with which it increased. Market changes feel uncomfortable when they happen quickly, even if the end result is not historically unusual.

Why This Episode Feels Different

Two features of the current market deserve particular attention. First, the pace of change has been unusually fast. Money moves more quickly than it once did, information travels instantly, and competitive advantages, especially in technology, can scale globally in a short period of time. Companies grow, and sometimes fade, faster than in prior decades.

Second, concentration today exists in tandem with elevated valuations. Markets have posted three consecutive years of strong growth. That does not mean stock values are extreme by historical bubble standards, but expectations are elevated. When optimism is embedded in prices, markets become more sensitive to disappointment. After three solid years, skeptics are looking for issues hidden under the surface.

Stock Market Mechanics Have Changed

If we take a step back from public stock markets, we may come to an unexpected conclusion – these companies aren’t so big after all.

There has been a major change in corporate finance over the last 15 years. In the past, the path to growth for most companies was to go public via an IPO and list shares on the major stock exchanges. This opened up access to capital that was otherwise unavailable to privately held companies.

The rise of private equity, venture capital and other alternative sources of investment changed the landscape. In fact, the number of U.S. companies traded publicly has fallen by nearly 50% since the 1990s.

Two of the largest IPOs in recent history were Visa, valued at $47 billion, and Facebook at $104 billion. These valuations are dwarfed by some of today’s private companies.

By year-end analysts expect SpaceX, OpenAI, and Anthropic to each go public and debut on U.S. stock markets. SpaceX and OpenAI are expected to carry market caps above $1 trillion, with Anthropic following behind in the $300-$500 billion range. If and when they are added to the S&P 500 Index, we will see natural dilution and broadening of markets.

Fundamentals Still Matter

One reason markets have tolerated high concentration is that today’s largest companies are not dominant in name only. They generate a disproportionate share of profits, cash flow, and economic value relative to their size.

As of early 2026, the top ten companies in the S&P 500 accounted for roughly 38% of the index’s market value, and 31% of total earnings. According to Russell Investments, the Mag 7 accounted for nearly 70% of the economic profit generated by S&P 500 companies. In short, the largest companies are the ones earning the most money, which is logical. While valuations for the largest firms are higher than for the rest of the market, their relationship to the rest of the market is in balance with historic norms.

Tech stocks dominating the headlines can remind some of the dot-com bubble of the late 90s. But the similarities are few. The dot-com bubble was marked by stocks like eToys, Pets.com, and others who earned valuations in the billions without ever turning a profit.

The Mag 7 companies are some of the most profitable companies in the history of the stock market. It remains to be seen how much of the recent AI spending frenzy is circular, and how much will lead to real economic growth. Neither the Mag 7 nor the rest of the market are cheap at moment, but today’s concentration is supported by real profitability rather than speculative mania.

Time will tell if the current valuations are overheated, but so far they are in line with their historical values relative to the market as a whole.

What Does this Mean for Long-Term Investors?

While concentration is not inherently dangerous, it can change how portfolios and markets behave.

As a larger share of market returns and volatility becomes tied to a small group of companies, diversification can become more fragile than it appears. When markets rise, gains come easily, but if a company or two stumbles, drawdowns can be sharper.

This is why advisors spend so much time on asset allocation in our portfolios, on aligning that allocation with the situation and needs of each individual, and on building portfolios that don’t simply mirror the market. We help you control your exposure to these concentrated companies by keeping a proper balance between them and the remainder of your investments.

Long-term investors know from experience that trends come and go, and that money is made by ignoring the short-term and harnessing the power of compounding over decades.

A Final Thought

Every era produces its champions, and every generation worries that this time is different. We’re biologically wired to be wary and look for signs of danger, even in times of prosperity. Occasionally, the cause for concern is real, but more often it’s a passing moment that has no lasting impact.

Today’s market leaders benefit from levels of innovation, profitability, and global scale that were largely unavailable to prior generations of companies. At the same time, high expectations and rapid change warrant careful monitoring.

In investing, clarity rarely comes from eliminating uncertainty. It comes from learning how to plan for it and live alongside it.

Presented by Christopher Rivers, CFP®, CRPC®