What is Tax-Loss Harvesting?

Tax-loss harvesting is when an investment is sold at a loss to help reduce your tax bill. This loss can be used to reduce other investment gains, and, in some cases, can also reduce other non-investment income. While we want investments to perform well, it’s an unfortunate reality that this isn’t always the case, and sometimes an investment is worth less now than when it was purchased. This is when “harvesting” tax losses can be a useful strategy to reduce your tax bill for the year. This strategy is especially relevant now with the market having pulled back from recent highs.

Think about someone who invested in the S&P 500 at the beginning of the year, which opened trading on January 2nd at $5,903.26, and at one point in March dropped to $5,521.52. This represents a decline of 6.5%. For every $100,000 invested, the position would’ve lost $6,500. If you’re in the top capital gains bracket, using this loss to offset other gains in your portfolio could result in Federal tax savings of about $1,500.

Why is Tax-Loss Harvesting Useful? It can be a great way to…

- Rebalance your portfolio

- Help with the process of selling your home

- Save the losses for a rainy day

If you have large, unrealized gains in concentrated positions, one way to reduce the risk is to sell some of your position and buy something new. This might leave you with a large tax bill, which can be offset by any losses that you have harvested. This is something we did frequently in 2020 and 2022, and while the market declines were temporary, it was a useful opportunity for us to rebalance portfolios for clients more cheaply than we could now.

An often-overlooked example of how tax-loss harvesting can be beneficial is when you’re selling your home. If you have a taxable gain when selling your home, you can use losses from your investments to reduce or even eliminate this gain. It becomes even more useful if you’re selling a second home, which doesn’t receive some of the same tax breaks that you get when selling your primary residence.

If your losses exceed your gains in the current year, all is not lost! Capital losses have an unlimited carryforward, meaning that if you have more losses than gains in the current year, the unused losses can be recorded on your return and used in a future year. It’s something we saw a lot in 2022, which was a tough year for the markets. In years when your losses exceed your gains, you can use up to $3,000 of losses to offset your ordinary income, which is an added benefit.

Things to consider:

- Tax-Loss Harvesting is not possible in retirement accounts

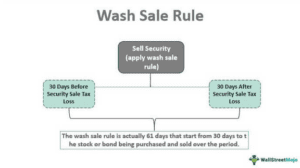

- Remember the wash-sale rule

- The risk of missing out on gains

- What you need to know about lowering your basis

- Not all states allow you to carryforward losses

While 401(k)s are taxed differently and can’t benefit from loss, the trades you make in these accounts can affect your ability to recognize losses from your other investment accounts. This is because the IRS disallows losses when you purchased the same or substantially identical investment either 30 days before or 30 days after the sale, which is known as a wash sale.

The reasoning is that the IRS doesn’t want you to sell the security for a loss and then immediately repurchase it, allowing you to take the deduction while avoiding any risk that the investment appreciates while you don’t hold it. Using Nvidia as an example, if we purchased the stock towards the end of last year, we would have the opportunity to sell it now for a loss. Say we wanted to repurchase it because we thought it was a good long-term investment. If we sold it now and bought it back right after, the IRS wouldn’t allow us to take the loss. However, if we waited until after the wash-sale period had passed, then we would be allowed to buy Nvidia and still take the loss when filing our taxes.

The IRS looks at your situation from a holistic standpoint, so you can’t get around it by selling the stock in one account and quickly repurchasing it in a different one. This adds some risk to the decision. Do we sell now and take the loss, potentially missing out on any gains for 30 days, or do we continue holding the security and forgo the loss?

The important thing to remember is that you aren’t prohibited from purchasing any investment for 30 days before and after, you just can’t purchase the same investment or something substantially identical. What is the IRS’s definition of substantially identical? While it’s descriptive for a stock, they don’t go into specifics for mutual funds and other investments that aren’t as straightforward, which is when it can be important to talk with a tax professional.

If you like the investment as a long-term holding and are temporarily selling to take the loss, it doesn’t necessarily put you in a better position. When determining a gain or loss on an investment, the reference point is how much you paid for the investment—also known as your basis. While you may get a loss in one year, you are lowering your basis in the investment when you repurchase it, so you will have a larger gain when you sell it in the future.

Final Takeaway

As with all financial decisions, tax-loss harvesting isn’t a one-size-fits-all approach. Just because you can take a loss doesn’t mean that you should. If you like your investments as long-term holdings, selling them – even temporarily – could result in you missing out on gains, especially with the IRS’s wash-sale window in play. This is when it becomes smart to look at your situation to determine if a real benefit can be realized in your portfolio, on your taxes, or hopefully both.

Presented by Josh Kaplan, CFP®, EA