Investors had to navigate an environment full of twists and turns in 2022. After hitting a new all-time high in early January, the stock market undertook a steady decline through October, before recovering a bit going to year-end. Interest rates rose rapidly for the first time in decades, and inflation hit levels not seen in nearly 40 years.

On the other hand, unemployment was near record lows and home values hit new highs. Oil prices, forecast to hit record highs in the wake of the invasion of Ukraine, actually moved lower for the year. As we turn the page into 2023, we wanted to take a fresh look at some key components of the economy and the markets, talk about where we’ve been, and where we might be headed.

Inflation

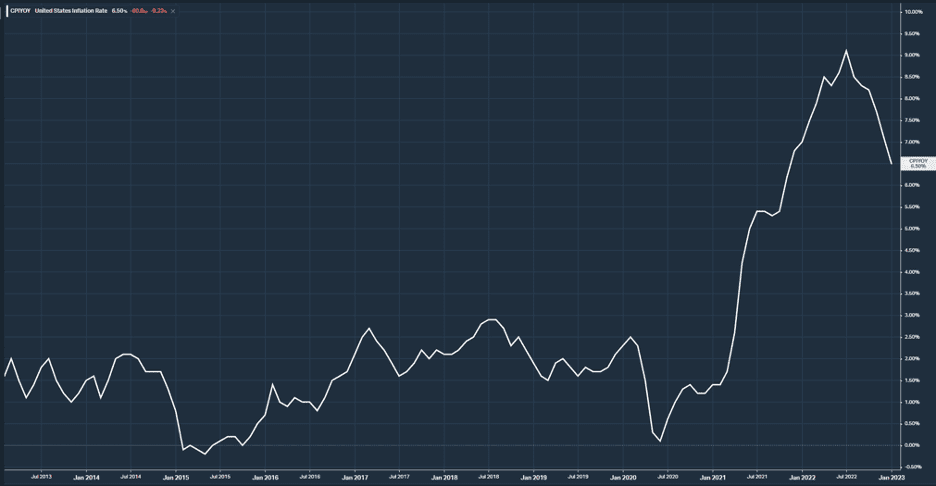

Inflation was the story of 2022, and the catalyst for many of the trends in the economy and the markets that we highlight below. You should be familiar with the general outline by now. Inflation began to rise in the 2nd half of 2021, prompting the Federal Reserve to begin 2022 with a campaign of rapid interest rate increases in an attempt to throw cold water on rising prices. Through the first half of 2022 inflation continued to rise, peaking at 9.0% in June.

As summer waned, we saw the first signs that rate hikes were working, and by year-end, the inflation rate stood at 7.1%, which was still elevated, but trending lower. The question for 2023 and beyond is how long it will take to get back to the Fed’s target of 2%, and how aggressive the Fed will be in pushing additional rate hikes to get there.

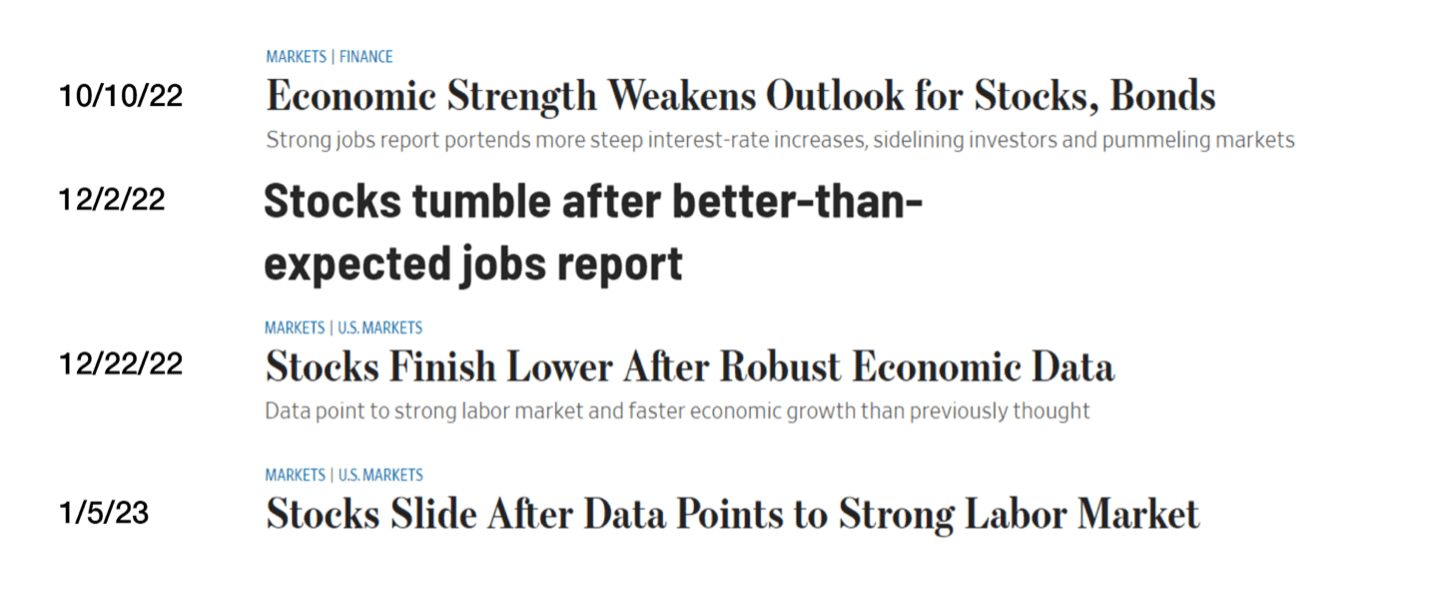

Good News Was Bad News In 2022

The Federal Reserve has two stated areas of focus: inflation and unemployment. With unemployment low and economic growth relatively stable, they felt empowered to make aggressive rate hikes to tame inflation.

As a result, particularly during the second half of 2022, we entered a somewhat strange cycle where good economic news was bad news for the investors. We regularly saw counterintuitive headlines like the ones above. The market seemed to interpret signs of economic strength as both a sign that inflation may remain high, and that the Fed would continue raising rates until they see inflation decline back to their target of 2%.

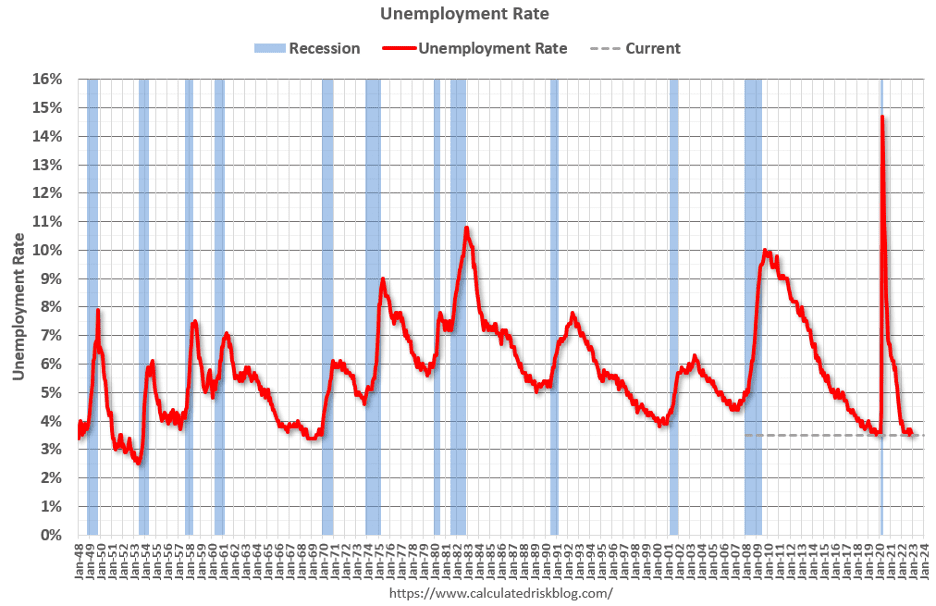

Unemployment

However, we have begun to see more frequent headlines announcing layoffs at some of the largest tech companies, including Microsoft, Amazon, Salesforce, Meta (Facebook), and Twitter. While these may be a signal that the job market is getting tighter, it’s important to keep these layoffs in context. While tech stocks make up a large part of the stock market, the market is not the economy.

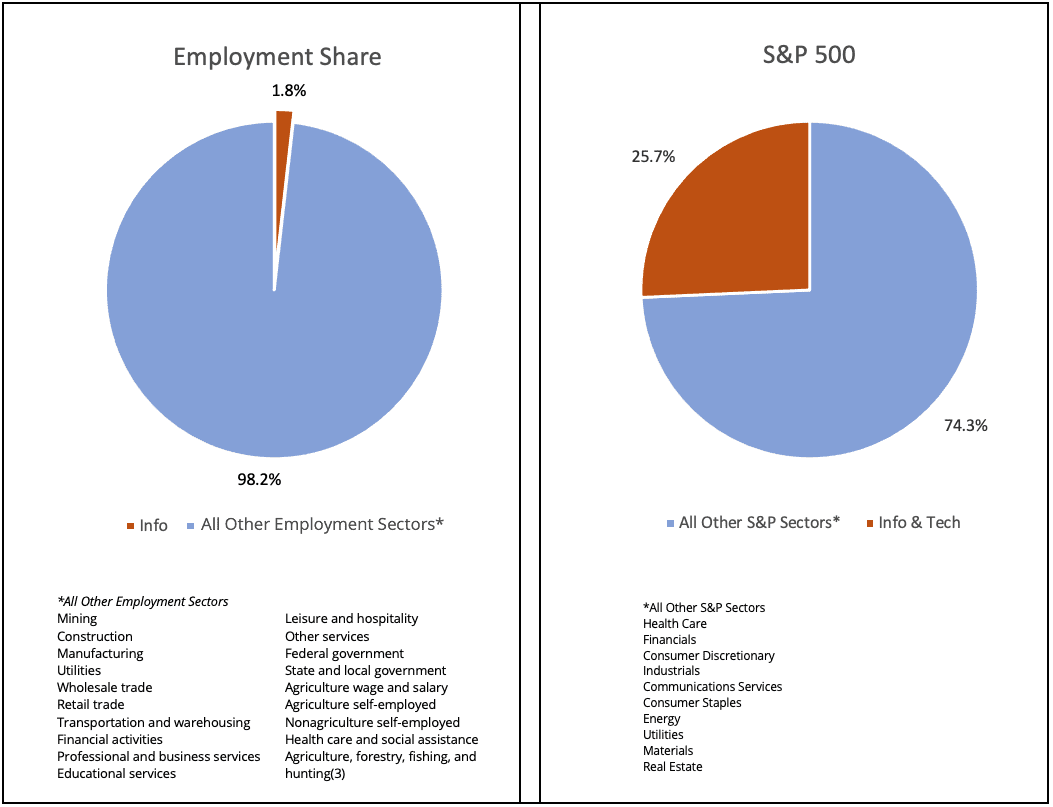

The Market is Not the Economy

So, while layoffs are never a good sign, tech layoffs may or may not be the canary in the coal mine. Tech companies employ a small workforce, relative to more labor-intensive industries like retail, healthcare, government, manufacturing, hospitality, and others. The companies and industries that are most important to the stock market don’t exactly line up with those most important to the job market and the economy.

The jobs story of 2020 was the complete wipeout of jobs in the hospitality and retail industries, while tech companies thrived. So, we may be seeing a bit of a rebalancing taking place, as traditional brick and mortar companies staff back up, and tech companies tighten their belts. In fact, we can see an echo of this if we look at the way markets performed in 2022.

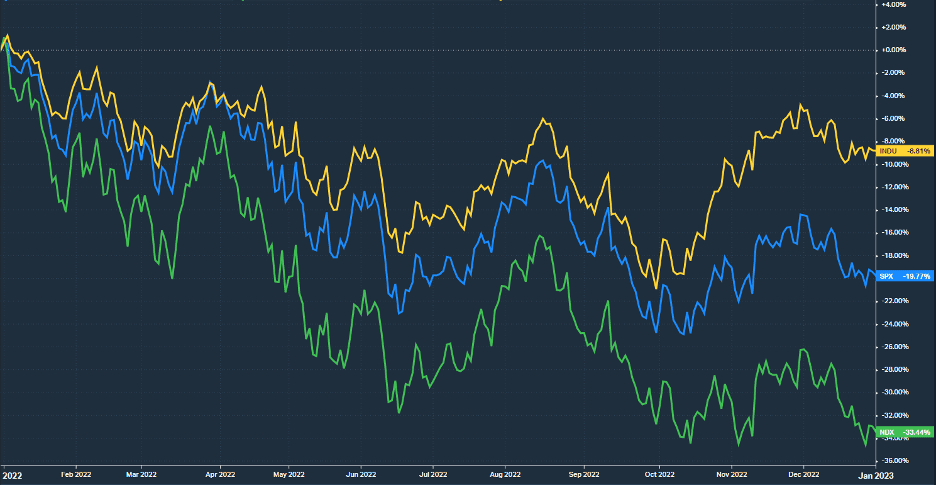

Markets Diverged in 2022

The Dow Jones Industrial Average, S&P 500, and Nasdaq are the most widely quoted measures of stock market performance. We’ve become accustomed to the Dow and the S&P moving in near lockstep over the past decade, while the more tech-focused Nasdaq tends to make similar moves, but with more volatility. However, in 2022 we saw a notable divergence, again illustrating how different parts of the economy are thriving or struggling.

In 2022, the Dow Jones posted a total return of -6.9%, the S&P 500 declined -18.1%, while the Nasdaq was down 32.5%. Here again, we see the tech vs. “real world” split. The Dow Jones is more heavily weighted to healthcare, financial services, and industrial companies, with tech making up just 14% of the index. The Nasdaq meanwhile is 49% tech, with the S&P splitting the difference at around 26%, as noted above. Many of the tech companies that enjoyed significant stock gains in 2020 and 2021 during the pandemic, saw their stock prices come back to earth in 2022. Meanwhile, traditional industrial and consumer facing companies saw more modest declines.

To be clear, the tech industry remains one of the most important cogs in the American economic machine, and the engine of much growth and innovation both here and abroad. But it remains to be seen whether the pain in the tech sector spreads to other industries.

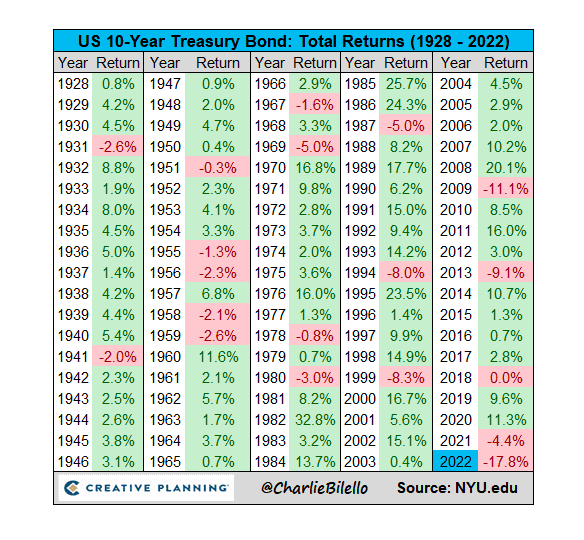

Bond Markets Sink, Dragging Portfolios with Them

As a result, diversified investors felt more pain than usual, as bonds—typically the conservative slice of their allocation—dropped in tandem with stocks. 2022 was the worst year for a “60/40 portfolio” since 1937, with a portfolio made up of 60% U.S. stocks (S&P 500) and 40% bonds (10-Year Treasuries) declining 18.0%.

Checking the Boxes on the March to Recession

We entered 2023 with a picture that was perhaps even cloudier than usual. On the surface, a low unemployment rate and solid 2nd half economic output showed resilience in the face of high inflation, a wobbly stock market, and a dreadful bond market.

However, towards the end of the year, we began to see underlying signs of weakness. While the unemployment rate was strong, wage growth began to slow, with December showing the smallest increase since August 2021. In addition, average hours worked dipped, and hiring in the service economy fell for the month.

This wasn’t the only cause for concern in the service industry. In December, the ISM Non-Manufacturing Index dropped to 49.6. A reading below 50 on this index indicates a contraction in the service industry, and this was a notable surprise, as forecasters had expected continued growth in December.

The warning signs aren’t isolated in the service economy either. In December, U.S. manufacturing output dropped 1.3%, following a 1.1% decline the previous month. Looking elsewhere, we see further signs of slow down. On the corporate side, profit margins across all industries peaked earlier in 2022. On the consumer side, after soaring for two years, housing prices declined significantly heading into year-end.

Consumer Remains Strong…For Now

While all of these industries are important, the great engine of the American economy is the consumer, with consumption typically around 66% of total economic activity in the U.S. Consumer spending has been resilient, as we can see above, but behind the headlines we are seeing some early signs of weakness. Retail sales dropped 1.1% in December, following a similar drop the month before. Consumer sentiment, meanwhile, hit a low not seen in 40 years.

The one area of continued strength is the jobs market, with nearly 1.8 job openings for every unemployed person. It appears that for now, jobs are the glue holding the economy together. If the jobs picture darkens, consumer spending tends to follow. One measure we will be watching in 2023 is weekly initial unemployment claims. Recent weeks have seen between 190,000 and 220,000 new jobless claims, again near 50-year lows. We often see these rise in advance of a recession, and if these were to rise above 300,000, we have greater concern a recession is on the horizon.

In short, we have begun to check some of the boxes on the march to recession. While by no means a certainty, the path to a “soft landing” without a recession has narrowed as we enter 2023. If the jobs market weakens, the path to a soft landing may be closed off entirely.

There is, however, a chance that should a recession come, it comes and goes with only modest impact. Our two most recent recessions (2020, 2008) are two of the worst on record, so it can be hard to think otherwise. But the prior two recessions in 2001 and 1991 were relatively mild. And the current economic situation is much more stable than the tech, terror, and debt fueled recessions from recent memory.

Charting A Course

Historically, markets tend to the lead the economy. We saw that play out in 2022, with the declines in stock and bond markets beginning perhaps a year before a potential recession. While a contraction in economic activity is by no means a positive for markets, it is important to understand the historical context. The market tends to bottom out before the economy does, and, on average, market recoveries have begun roughly two-thirds of the way through a recession.

In fact, in a number of recessions – 1960-61, 1980, 1982, 1991 – the S&P 500 actually posted gains for the duration of the recession. We may not be so lucky this time, but a recession does not ensure a market meltdown. This highlights again the value of a balanced portfolio in service of a financial plan.

It can be hard to balance our concern for the country and the economy with our viewpoint as investors. With a plan in place and short-term needs accounted for, the long-term investor can avoid temptation to do something when the most profitable course of action has been to remain patient.

What happens is out of our control, but how we respond is our choice. The long-term investor, with a financial plan in place, has the luxury of waiting out the economic cycle, and perhaps turning it to their advantage by investing when the market goes on sale.

Whether the market drops further and goes “on sale” in 2023 remains to be seen. But for most, this should be nothing more than a bumpy stretch on a long and winding journey