Creating a budget can be a challenge even in the calmest of times, so how do you begin to tackle it in an uncertain epidemic environment? Fortunately, the individual line items you would normally take into consideration are fundamentally the same – even if the allocation of funds to each may have shifted.

Back to Basics

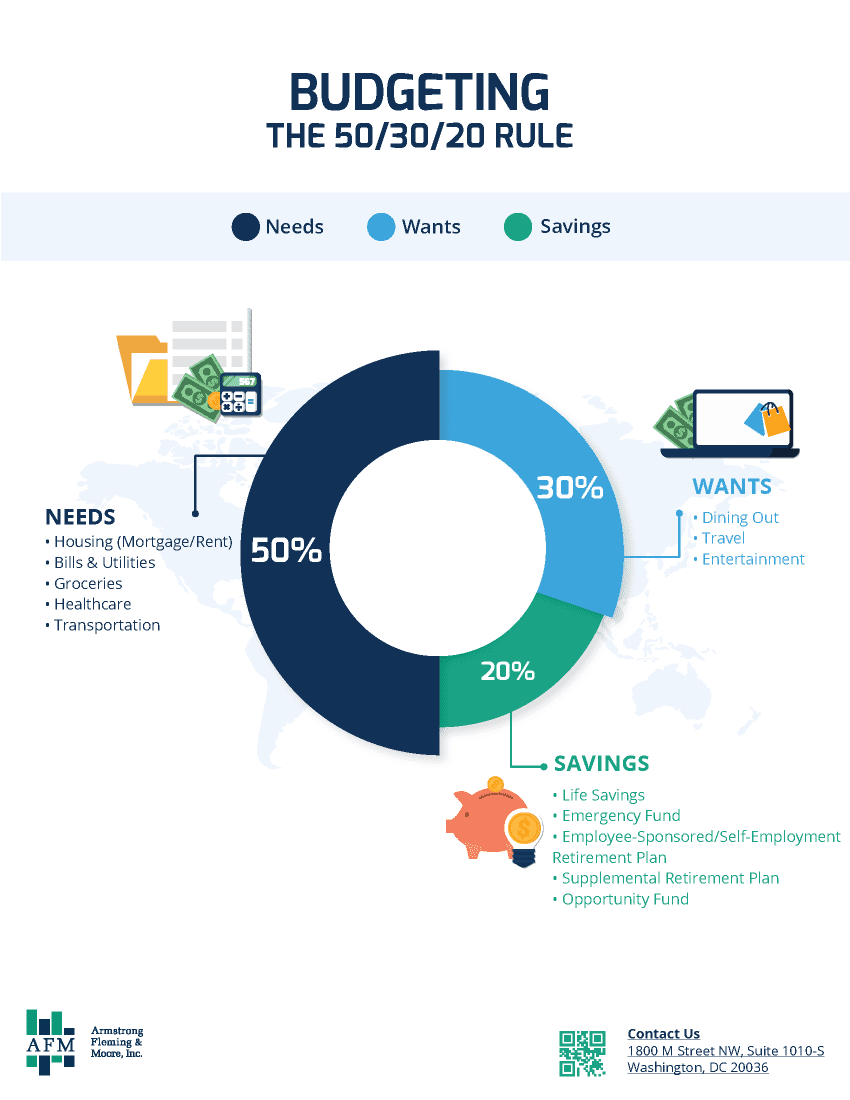

When approaching your budget, whether for the first time or just the first time in a long time, it helps to start from a standard framework rather than trying to build from scratch. For example, a common starting point is breaking down your after-tax income into the 50/30/20 model where 50% covers Needs (housing, groceries, utilities, and minimum required debts payments), 30% covers Wants (entertainment, travel, new gadgets), and 20% covers Savings and Debt repayment (any additional payments made towards the principal balance, beyond the required minimums).

Once you have ballpark figures, you can address your individual needs and reallocate to suit your lifestyle. Maybe your beloved dog needs costly medications to maintain their quality of life so your Needs bucket increases by 5% and you’re happy to reduce your Wants funding by 5% to care for your furry friend. Perhaps you depend on a particular gym community for not only your physical health but also boosting your mental health – cooking at home regularly rather than ordering takeout may build space in your cash flow to comfortably sustain the cost of your membership.

The details of each person’s budget can vary widely and may be heavily influenced by your current life stage. Allow yourself some level of flexibility on the exact percentages of your 50/30/20 template. Things will most likely shift depending on your unique combination of income, student debt, housing needs, medical conditions, and family dynamics – just to name a few. We typically encourage working towards the 20% Savings goal over time to build your emergency fund, pay down your debts, and grow long-term goal reserves.

Into the Weeds

Once you have your basic structure in place, you can dig further into the specifics of your spending and income to determine where COVID repercussions may most significantly impact your present and future finances.

If you’ve been saving towards a down payment on a new home, the aggressive seller’s market and rising mortgage interest rates almost guarantee you will be paying more than anticipated in both upfront costs and monthly repayments. In response, do you rein in other elements of your spending? Or do you find a home that isn’t as turnkey as your ideal choice and commit to updating the space to your tastes over a longer period?

Dying to break out of the four walls that you and your family have been living, working, eating, and sleeping in for the past two years? Paying for airfare, hotels, and meals out for a family might come with sticker shock. Would you consider renting or purchasing an RV to hit the road and visit the National Parks this summer instead?

Even your weekly grocery list may need a quick revision as inflation and supply chain challenges increase the costs of common products.

Think outside the box

While much of the time spent budgeting focuses on how to thoughtfully reduce your spending and allocate your current income, you may also want to assess how you could increase your income to help reach your goals. Perhaps professional certification or a graduate degree could increase your expertise in a field or allow you to shift onto another career path that provides a higher level of income and benefits. Alternatively, changing jobs and relocating to an area with a lower cost of living, or where you have a support network to assist with childcare, may serve to close gaps between your income and expenses.

Regardless of your situation and goals, it’s easier to get where you’re going if you have a plan. If you’re struggling to find your financial path, or just can’t focus through the COVID fog we’ve all been living under, consider reaching out to us to discuss how we may be able to help.