2024’s massive election year, in which over 70 countries are holding elections, is coming to a head for us as we approach November 5th. And if we look at recent history, the result of the election is unlikely to be decided that night. Four years ago, we had a similar election to then President Donald Trump and the future president in Joe Biden. Now, it’s Trump and Kamala, with parties divisive as ever. So as we think about what will happen to the markets, it’s easy to grow nervous, even scared. But how did we get here? Chris Fasciano, senior portfolio manager, at Commonwealth Financial Network® explains below.

The Election Season Rollercoaster

The first presidential debate took place on June 27, with President Biden’s performance coming under scrutiny from the media and the Democratic Party. This was followed in short order by an assassination attempt on former President Trump, then the Republican National Convention, and the nomination of the Trump-Vance ticket. Three days later, President Biden announced that he would not seek reelection. The party quickly rallied around Vice President Harris as the presumptive nominee. She chose Minnesota Governor Tim Walz as her running mate, and the Harris-Walz ticket was officially nominated at the Democratic National Convention in late August. Through it all, the polls at the national level and in some of the key toss-up states have shown considerable volatility.

Of course, no one knows who will prevail in this presidential contest. But there are several things we do know. Recent history dating back to 2000 suggests the race will be tight, with vote counting taking time. Ultimately, the election will likely be decided by a handful of swing states.

Will the Election Affect Your Portfolio?

You may wonder how a Democratic or Republican winner could ultimately affect the markets and economy. Indeed, there are policy differences between the two candidates, most notably in their views on the expiration of the Trump tax cuts.

The Tax Cuts and Jobs Act (TCJA). The TCJA, which became law on January 1, 2018, was the largest change to the tax system in three decades. There are many different pieces to this legislation, but the biggest provisions set to expire at the end of 2025 are:

-

- Lower individual tax rates

- A higher standard deduction

- An increase in the child tax credit

Despite being signed into law by former President Trump, some of these issues are also important to Democrats.

Here’s the bottom line: Regardless of who ends up in power, it’s unlikely that all of these tax benefits will completely go away. The impact on the market and economy will depend on which issues the new Congress and the administration prioritize. Still, it’s important to remember that big changes require one party to have control of both the White House and large majorities in Congress. Even with one party in charge, there are many different views within the party that can make passing new laws difficult in today’s political environment.

Now, all of this may sound like the election result will have a major impact on our day-to-day lives and the U.S. economy, potentially creating ups and downs in the stock and bond markets. We might think there are things to worry about that could lead to big changes in how we manage our investments in response to the potential political risk. But will it really have such a big impact? And do we need to change our investment strategies?

Portfolio Changes Ahead?

At a high level, we wouldn’t suggest any major changes to a balanced and diversified portfolio if we knew the election results ahead of time. In the meantime, we may watch for short-term market reactions to election news, which might create attractive long-term investment opportunities. Short-term market moves based on campaign headlines tend to be based on emotions, not fundamentals. That could potentially cause short-term sell-offs in various investments that provide good entry points for long-term investors willing to look past the noise. A look back at recent history can help explain.

The Story of Elections Past

Although the president is arguably the most powerful person in the world, they don’t singlehandedly determine the path of economic growth or the markets’ reaction to the data. Figure 1 illustrates that, over time, the economy has grown. And most years? The markets have also gone up.

Figure 1. Party Control and the Path of Economic and Market Growth

As you can see in the second chart above, dating back to the Truman presidency (1945–1953), every president has been in office during at least one year when the S&P 500 had a negative return. The exception to this is President Obama, who took office in 2009 at the end of the great financial crisis bear market.

Market timing studies have consistently concluded that knowing what will happen just before an election and investing accordingly is very hard—if not impossible—to do. As such, it is difficult to adjust portfolios based on an event with an unknown outcome, followed by uncertainty as to how the result will be implemented over the next four years.

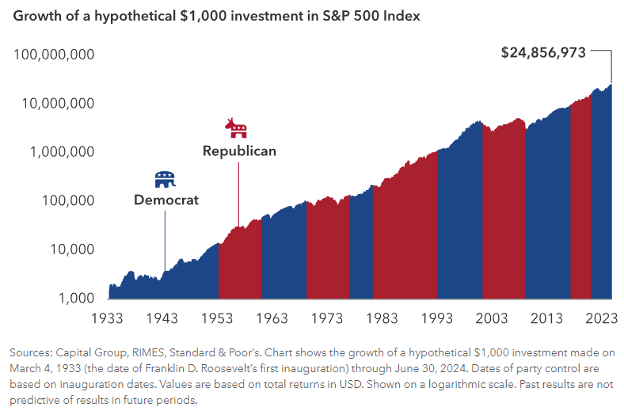

In the long term, the power-sharing agreement in Washington doesn’t matter much to markets and investors. Figure 2 illustrates that a long-term time horizon without regard to the party affiliation of the president in the White House has yielded strong returns for investors.

Figure 2. Growth of a Hypothetical $1,000 Investment in the S&P 500 Index

Given this data, we believe it makes sense to adhere to a long-term view that achieves a client’s investment objective and to stick to a portfolio process that results in balance and diversification. This approach could ride out any potential short-term market volatility that results from election noise.

Looking Forward

We fully appreciate that the election will continue to be on many clients’ minds over the rest of the year. But despite concerns and potential market volatility, our advice is always and continues to be this: vote in the booth, not in your portfolio.

Authored by Chris Fasciano, senior portfolio manager, at Commonwealth Financial Network®.

Certain sections of this commentary contain forward-looking statements based on the reasonable expectations, estimates, projections, and assumptions from Commonwealth Financial Network. Forward-looking statements are not guarantees of future performance and involve certain risks and uncertainties, which are difficult to predict. Opinions are subject to change without notice. Past performance is not a guarantee or indicative of future results.

This communication should not be construed as investment advice, nor as a solicitation or recommendation to buy or sell any security or investment product. Diversification does not assure a profit or protect against loss in declining markets. Investments are subject to risk, including the loss of principal and there is no guarantee that any investing goal will be met. All indices are unmanaged, and investors cannot actually invest directly into an index. Unlike investments, indices do not incur management fees, charges, or expenses

Commonwealth Financial Network® and Armstrong, Fleming & Moore do not provide legal or tax advice. You should consult a legal or tax professional regarding your individual situation.

© 2024 Commonwealth Financial Network®